History of GST in India

Bio

Shreyansh Singh, an IIT Kanpur alumnus, has eight years of experience in the finance industry. He has spent 5 years at American Express developing mid to long-term strategies for multiple markets including US, Europe and India. Shreyansh currently leads Growth and Strategy initiatives at Pice.

- 16 Sep 24

- 12 mins

Share

History of GST in India

- 08 Mins

- 16-09-24

Table of Contents

Share

Key Takeaways

- GST unified India's indirect taxes on July 1, 2017.

- Initiated in 2000, GST overcame many legislative hurdles.

- Introduced CGST, SGST/UTGST, and IGST on goods and services.

- GSTN digitized tax procedures, reducing evasion.

- Created a unified market, lowered taxes, and boosted economic growth.

In the dynamic world of taxation, the introduction of the Goods and Services Tax (GST) marks a significant shift in India’s tax system. GST is a unified tax imposed on goods and services throughout their journey from production to final consumption, effectively replacing all previous indirect taxes.

This article explains into the history of GST in India, tracing its journey from the initial concept to its present structure and exploring the substantial changes it has brought to the Indian economy.

Legislative Milestones on the History of GST in India

In May 2015, a significant moment in India's tax history occurred when the Constitution (122nd Amendment) Bill was successfully passed in the Lok Sabha, marking a key step in the journey towards implementing GST. After this approval, several essential bills were introduced to prepare for the official launch of GST on July 1, 2017. These included the Union Territory GST Bill, the Central GST Bill and the GST (Compensation to States) Bill.

Each of these legislative actions played a crucial role in establishing the foundation for the GST system, which aimed to simplify and unify India's indirect tax structure. This series of events highlights the extensive efforts and legislative progress that led to the successful implementation of GST in India.

When Was GST Implemented in India?

GST was first implemented in India in 2017, marking a significant change in the country's tax system. However, the history of GST dates back to 1954, when France became the first country to adopt it. Since then, over 160 countries have followed suit, with Malaysia being one of the latest to implement a value-added tax system in 2015. In its journey through the history of GST, India chose a dual tax structure to streamline and modernise its indirect tax system.

Who Was Behind the Introduction of GST in India?

The introduction of GST in India was led by then Finance Minister Mr Arun Jaitley. He brought the Constitution Amendment Bill to the parliament in 2014. Following this, the Constitution (122nd Amendment) Bill was passed in the Lok Sabha in May 2015. By April 20, 2017, key bills such as the Integrated GST Bill, the Union Territory GST Bill, the Central GST Bill, and the GST (Compensation to States) Bill had successfully passed through both the Lok Sabha and the Rajya Sabha. GST was officially launched across India on July 1, 2017.

History of GST in India

?feature=shared

?feature=shared

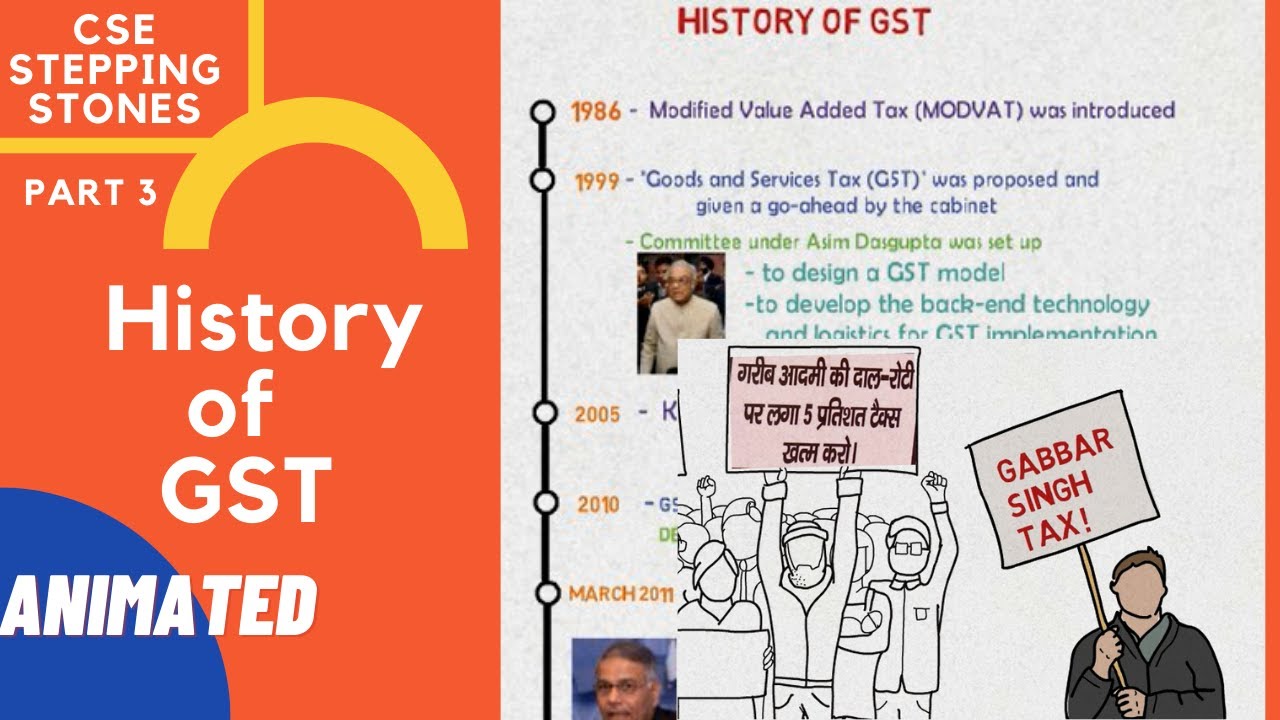

The history of GST in India started more than two decades ago in the year 2000 during the rule of the Atal Bihari Vajpayee government. The initial talks regarding the implementation of GST occurred, culminating in the creation of an empowered committee of state finance ministers, many of whom had prior experience with State VAT. In 2004, the Fiscal Responsibility and Budget Management Committee was formed and it suggested the implementation of GST.

During the presentation of the 2006-07 Budget Speech, the Union Finance Minister said that GST will be rolled out by April 1, 2010. However, because of some factors, the introduction was affected and thus, delayed. In 2011, the Constitution (115th Amendment) Bill was introduced in parliament to include certain GST provisions and was thoroughly reviewed by a Standing Committee.

Upon its implementation, GST replaced several central taxes, including:

- Service tax

- Cess and surcharge

- Excise duties

- Central excise duties

- Additional duties of customs

- Additional duties of excise

GST also subsumed several state taxes, such as:

- State VAT

- Entry tax

- Central sales tax

- Purchase tax

- Luxury tax

- Entertainment tax

- Taxes on advertisements

- State cess and surcharges

- Taxes on gambling and lottery

Delays and Challenges in GST Implementation

The Constitution (115th Amendment) Bill, 2011, was introduced but became invalid when the Lok Sabha was dissolved in 2014. This led to the need for a new Constitutional Amendment Bill.

The Formative Years

- 2000: The establishment of an empowered committee of State Finance Ministers.

- 2006: Finance Minister P. Chidambaram announced that GST would be introduced soon.

- 2009: The Empowered Committee released India’s first discussion paper on GST.

- 2010: President Pranab Mukherjee postponed the GST launch to April 2011.

Legislative Developments

- 2011: The Constitution (115th Amendment) Bill was introduced.

- 2013: The Standing Committee on Finance presented a detailed report.

- 2014: The Lok Sabha’s dissolution caused the Bill to lapse.

- 2015: The Constitution (122nd Amendment) Bill was passed and sent to a Select Committee in the Rajya Sabha.

Turning Points

- 2016: The Bill was passed by both the Lok Sabha and the Rajya Sabha, becoming the Constitution (101st Amendment) Bill.

- Assam was the first state to ratify the Bill.

- President Pranab Mukherjee gave his assent.

- The GST Council was formed and held its first meeting in New Delhi.

GST Era

- 2017: The IGST, CGST, UTGST, and SGST (Compensation to States) Bills were introduced, and GST was officially implemented on July 1.

- 2018: TDS provisions and the E-way bill system were introduced.

- 2019: The reverse charge mechanism was implemented, and restrictions on availing input tax credit (ITC) were introduced.

- 2020: E-invoicing and a quarterly return monthly payment scheme were introduced.

- 2021: New updates included GSTR-8, GST on services through e-commerce operators, and GST on services provided by state governments to their own undertakings.

Tax Structure Before GST

Before GST, the tax system was straightforward but separate: the central government and state governments each had their own taxes without overlap. The central government taxed goods manufactured in factories, though this did not include alcohol or pharmaceuticals. While the states levied taxes on the goods that were traded within their jurisdiction. In addition, the central government levied a tax on the movement of goods from one state to another, which was paid to the state of destination.

The central government also levied taxes on a number of services and not only on products. Furthermore, there were other taxes when goods were imported into or exported out of India such as the CVD and SAD taxes, in addition to the customs duty. These extra taxes were supposed to equalise other taxes such as excise duties and state VAT.

The rules of taxation changed with the implementation of GST wherein both the central and state government can tax the goods and services at the same time. This made them sit down and agree on how GST would be implemented in order to be fair and well-organised in the implementation of the tax system.

Decisions Taken by the GST Council

The GST Council has made several significant decisions:

- They established four primary GST rates: 5%, 12%, 18%, and 28%. Some items are exempt from any tax.

- An additional tax, above 28%, is applied to luxury goods and products like tobacco.

- State tax authorities bear 90% of the tax obligations of firms with an annual turnover of less than ₹1.5 crore and the rest 10% is borne by the central government.

- For businesses earning over ₹1.5 crore annually, both state and central tax authorities share the tax responsibilities equally.

- To support the functioning of the GST, the government formed GSTN in 2013 in the form of a private limited company. It is an online portal through which business entities can apply for GST registration, remit taxes and submit returns. GSTN also designs the software for 25 states that are part of the system.

- GSTN collaborated with 34 technology and finance companies to develop apps and tools that help businesses manage their GST tasks online more efficiently.

Features of the GST Regime

The GST system has revolutionised the taxation of goods and services in India with its unique and comprehensive approach:

- GST Application

Unlike the old tax system, GST is applied to the 'supply' of goods and services. This means that GST is levied whenever goods or services are transferred or provided, rather than focusing solely on manufacturing or sales.

- Destination-Based Tax

GST is charged based on where goods or services are consumed or used, rather than where they are produced. This ensures that tax is paid in the place where the goods or services are finally consumed.

- Three-Part Tax Structure

GST comprises the following three parts: CGST which stands for central GST, SGST/UTGST which stands for state GST or union territory GST and IGST which stands for inter-state GST. The tax slabs of IGST are determined by both the central and the state governments.

- Central Taxes Replaced

GST has subsumed several central levies including excise duties on commodities like medicine and toiletries, service tax and customs like CVD – Countervailing Duty and SAD – Special Additional Duty.

- State Taxes Consolidated

Several state taxes have been merged under GST, including VAT (Value Added Tax), entry taxes, luxury taxes and entertainment taxes (excluding those collected by local bodies). This consolidation simplifies the tax system and reduces complexity.

- Exemptions for Small Businesses

Small-scale businesses with an annual turnover of less than ₹20 lakh are not required to pay GST and hence the pressure is not much on them. For the businesses located in the special category states, this limit is ₹10 lakh. Further, the GST Council has provided an option of a composition scheme for turnover up to ₹50 lakh where the registered business has to pay GST at a fixed rate making it easy for compliance.

- Specific Use of Tax Credits

As seen in the GST system, the CGST credit can only be utilised against CGST liability and the SGST/UTGST credit can only be used against the SGST/UTGST liability. However, credits from any of the categories can be utilised for payment of IGST which has made it easier to deal with tax issues of cross-state transactions.

By addressing the issues and complexities of the previous tax system, GST aims to create a more streamlined, efficient and fair tax structure in India, encouraging economic growth and reducing tax evasion.

Benefits of GST Implementation

The introduction of GST in India has brought about several key benefits:

- Unified Market: GST has created a single, unified market across India, making the country more appealing for foreign investments by eliminating various state-specific taxes.

- Reduced Tax Burden: It has reduced the ‘tax on tax’ situation, hence reducing the cost of doing business for business entities as well as the consumers.

- Standardised Regulations: GST has brought uniformity in the tax system including the laws, rates and procedures throughout the country, thus easing business transactions for companies dealing across states.

- Economic Growth: The new tax system is expected to stimulate manufacturing and exports, creating jobs and fostering economic growth.

- Competitive Pricing: Indian products can now compete more effectively in global markets due to a streamlined tax structure.

- Enhanced Investment Climate: GST is likely to make India a more attractive destination for investments.

- Reduced Tax Evasion: The uniformity of SGST and IGST rates makes tax evasion more difficult, increasing revenue collection.

- Lower Business Costs: It is anticipated that costs will decrease for the companies, which in turn will lead to increased consumption and production.

- Simplified Tax System: GST provides a simpler structure of taxation with a very limited number of exemptions as compared to previous taxes which makes it easier to deal with.

- Digital and Streamlined Procedures: Registration, tax payments, returns and refunds under GST are streamlined and can be done online through the GSTN.

- Transparent Input Tax Credit: The method of claiming input tax credits is more precise and clear as compared to the previous system and less chances of fraud are there.

- Lower Product Prices: The efficient input tax credit mechanism under GST assists in making the final price of the product affordable to the consumers.

- Support for Small Retailers: Small-scale retailers may be exempt from GST or benefit from lower rates, making essential goods more affordable.

Must reads

Conclusion

The history of GST in India reflects a transformative journey from a complex tax system to a unified and efficient structure. It replaced a range of outdated taxes with a streamlined approach, facilitating easier compliance and reducing tax burdens.

By creating a single market across India, GST has promoted economic growth, enhanced competitiveness and simplified business operations. Furthermore, its ongoing adjustments and improvements will continue to shape India’s tax system.

💡If you want to streamline your payment and make GST payments, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

What is GST and when was it implemented in India?

The Goods and Services Tax (GST) is a comprehensive, multi-stage, destination-based tax that unified India's indirect tax system by replacing multiple central and state taxes. It was officially implemented across the country on July 1, 2017. GST aims to streamline taxation by applying a single tax on the supply of goods and services from the manufacturer to the consumer, creating a unified national market.

How did GST change the taxation system in India?

GST revolutionized India's taxation by consolidating various central and state taxes like excise duties, service tax, VAT, and others into a single tax system. It introduced a three-part structure comprising CGST, SGST/UTGST, and IGST, applicable on the supply of goods and services. This shift eliminated the cascading effect of taxes, reduced the overall tax burden, and simplified the tax compliance process for businesses.

What are the different components of GST?

GST consists of three main components:

CGST (Central GST): Collected by the Central Government on intra-state sales.

SGST/UTGST (State GST/Union Territory GST): Collected by State Governments or Union Territories on intra-state sales.

IGST (Integrated GST): Collected by the Central Government on inter-state sales and imports.

This structure ensures both central and state governments receive their share of taxes, promoting cooperative federalism.

CGST (Central GST): Collected by the Central Government on intra-state sales.

SGST/UTGST (State GST/Union Territory GST): Collected by State Governments or Union Territories on intra-state sales.

IGST (Integrated GST): Collected by the Central Government on inter-state sales and imports.

This structure ensures both central and state governments receive their share of taxes, promoting cooperative federalism.

What were the challenges faced during the implementation of GST?

Implementing GST faced several challenges, including legislative hurdles requiring constitutional amendments and consensus among states. Delays occurred due to political differences and the need for extensive coordination between central and state authorities. Businesses had to adapt to new compliance requirements and upgrade their accounting systems. Initial technical glitches with the GST Network (GSTN) portal also caused difficulties in registration and return filing.

What are the benefits of GST implementation in India?

GST has brought numerous benefits, such as creating a unified national market and making India more attractive to foreign investors. It reduced the 'tax on tax' effect, lowering the cost of goods and services. Standardized regulations have simplified interstate business operations. GST is expected to boost economic growth by enhancing manufacturing and exports, increasing competitiveness of Indian products globally, and fostering a transparent and efficient tax system.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

Related Articles

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction