Know the Key Difference Between Credit Note and Credit Invoice

Bio

Ankit Rahangdale is a seasoned finance professional with a distinguished background as a Chartered Accountant. Currently, he leads the Finance Department at Pice. With over five years of invaluable experience in the banking and finance sector, honing his expertise through esteemed institutions such as ICICI Bank and Standard Chartered Bank.

- 18 Nov 25

- 6 mins

Share

Know the Key Difference Between Credit Note and Credit Invoice

- 08 Mins

- 18-11-25

Key Takeaways

- The difference between credit note and credit invoice lies in their purpose, credit notes adjust overpayments or discounts, while credit invoices address faulty or returned goods.

- Credit notes must be declared in GSTR-1 by the earlier of 30th September of the following financial year or the filing date of the annual return.

- A credit note is issued when goods are not expected to be returned, mainly to adjust customer accounts for overbilling, rebates or discounts.

- A credit invoice is issued when goods are returned or billing errors need correction, enabling accurate refund and inventory adjustments.

- Proper understanding of the difference between credit note and credit invoice ensures correct GST reporting, compliance, and strengthened customer relationships.

Do you know you need to declare issuance of credit notes in GSTR-1 on the earlier of the following dates: 30th September of the year following the supply or the actual date of filing annual return?

However, here comes a common mistake that several taxpaying businesses make: they confuse credit notes with credit invoices. While they might sound similar, they are not the same.

Thus, learn the difference between a credit note and a credit invoice before you declare in your GST return.

What Is a Credit Note?

Suppliers issue a credit note or credit memo to customers, mentioning the credit for goods and services that are not expected to be returned. As a supplier, you can issue a credit note for overpayment, rebates, discounts and promotions.

You can use a credit note to maintain accounting records and track adjustments to account balances and customer refunds. As a supplier, you can further use a credit note to rectify discrepancies in billing, thereby establishing a positive relationship with customers.

What Is a Credit Invoice?

Suppliers issue a credit invoice to customers for money owed for faulty or returned goods, discrepancies in pricing or damaged deliveries. Businesses use credit invoices to rectify invoice errors in the billing system and enhance the relationship with customers.

These invoices are crucial to manage, track and report business finances. You can use these invoices to reconcile and maintain accurate sales records and transactions. This includes refunded, cancelled and returned goods.

You can further use a credit invoice prepared by the accounts payable department to adjust the outstanding balance of customers and accounts receivable by suppliers. Here is the key information that a credit invoice should contain, similar to an original invoice:

- Business details of the seller and the buyer

- Credit invoice number

- Date of issue

- Original invoice number

- Adjusted total amount and tax

- List of goods and services for credit

Must reads

Difference Between Credit Note and Credit Invoice

| Parameters | Credit Note | Credit Invoice |

| Purpose of Issuance | Issued to inform customers about the money they owe to suppliers without an expectation of goods being returned | Issued in the case of faulty or returned goods for money owed |

| When Is It Created? | When overpayment or discount is applied to the customer’s account | If a customer requests to rectify billing errors |

| When Is It Issued? | When the supplier wants to request payment | After a payment has been made |

When Are Credit Invoices and Credit Notes Used?

If a customer returns goods to the supplier and the latter agrees to refund the money, the supplier needs to issue a credit invoice. For instance, Mr X is a customer who returned goods worth ₹2,000 to supplier Mr Y. Then Mr Y will issue a credit invoice of ₹2,000 to refund the amount.

On the flip side, if a customer purchases goods from a supplier and the goods are not expected to be returned, the supplier will issue a credit note. For instance, Mr Z is a customer who purchased goods worth ₹5,000 from supplier Mr P. If the goods are not expected to be returned, Mr P will issue a credit note of ₹5,000 to request payment from Mr Z.

Use of Credit Invoices and Credit Notes with Examples

Different businesses use credit invoices and credit notes for overpayment, refund for returned goods and other purposes. Here is how businesses in the retail industry and e-commerce industry use these documents:

Credit Invoices in the Retail Industry

Suppose a customer, Mr A, returned purchased goods worth ₹1,000 because of defects to retailer Mr B. Mr B will issue a credit invoice to confirm refunds for returned goods. This boosts inventory management while ensuring customer satisfaction.

Credit Notes in Financial Services

For instance, suppose a client was billed ₹10,000 instead of the correct amount of ₹9,000 due to a calculation error. To fix this, the firm issues a credit note of ₹1,000. This not only adjusts the overcharged amount but also ensures transparency and maintains trust in the business relationship.

Must reads

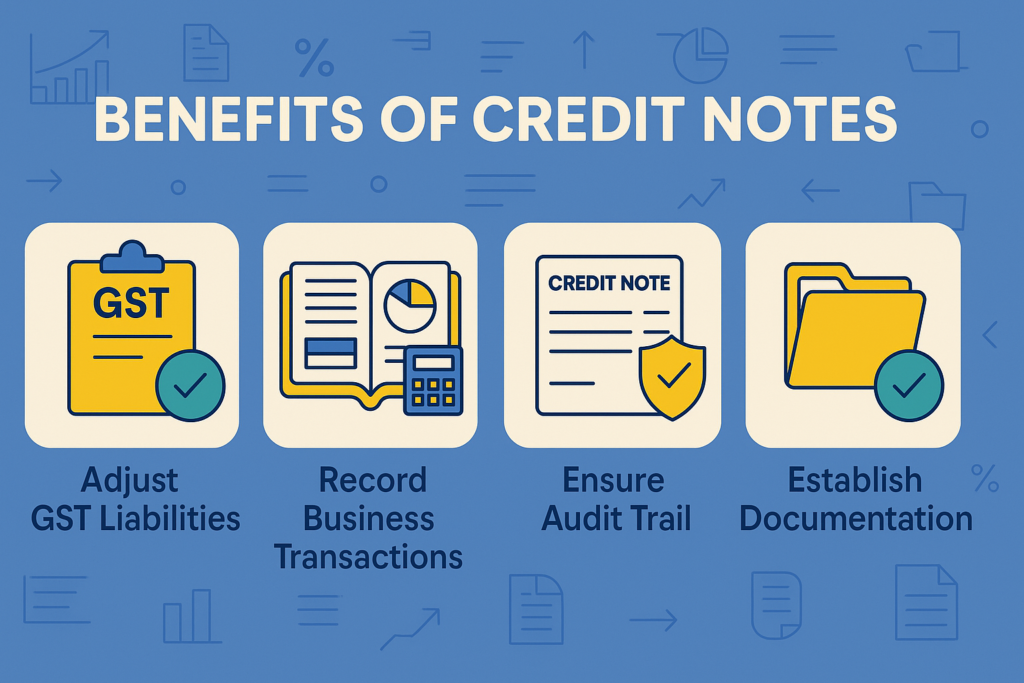

Benefits of Credit Notes

- Credit notes help adjust GST liabilities for taxpayers according to payment terms.

- It helps taxpayers comply with GST laws by keeping a record of business transactions and accounting documents.

- Credit notes ensure relevant documentation for tax audit trail.

Benefits of Credit Invoices

- It helps amend errors in the original invoice thereby rectifying financial records or financial documents.

- Credit invoices help keep customers’ accounts updated with accurate cash flow details in the accounting system.

💡For your bill payments and tracking business transactions, use the PICE App.

Conclusion

Now that you are clear on the difference between a credit note and a credit invoice, you are less likely to confuse the two. Make sure to declare your credit notes accurately in GSTR-1. Timely and correct reporting not only ensures compliance but also helps you avoid penalties.

FAQs

What is the main difference between credit note and credit invoice?

A credit note adjusts overpayments or discounts, while a credit invoice adjusts refunds for returned or faulty goods.

When should a credit note be reported in GSTR-1?

By the earlier of 30th September of the next financial year or the annual return filing date.

Who issues a credit note?

The supplier issues a credit note to record adjustments like discounts, rebates or billing errors.

Why is a credit invoice issued?

It is issued when goods are returned or when the original invoice contains errors needing correction.

Why is understanding the difference between credit note and credit invoice important for businesses?

It ensures accurate GST compliance, proper accounting, and correct financial adjustments.

Read More About Invoice

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

Related Articles

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction