Financial Credit Note Under GST

Bio

An Alumnus of IIM and DU with almost a decade of experience in the banking and finance sectors. I had the opportunity to work with all types of institutions in BFSI ecosystem like Bank, NBFC, Fintech, Consulting and Auditor. I started my professional journey at KPMG and subsequently worked in leading names of the BFSI sector including Ujjivan Bank, Vistaar Finance. Currently building a fintech startup ( PICE) by handling alliances, compliance and creation of GTM strategy for payments and credit product.

- 9 Sep 24

- 7 mins

Share

Financial Credit Note Under GST

- 08 Mins

- 09-09-24

Key Takeaways

- A financial credit note is issued by suppliers to adjust taxable supply values due to reasons like discounts, product returns, or discrepancies in invoicing.

- Credit notes help correct overcharges or damaged goods and must include key details like the supplier's GSTIN, taxable amount, and tax rate.

- Credit notes must be reported in GST returns to adjust tax liabilities, ensuring transparent tax filings.

- There is no specific format for a credit note under GST, but essential information like a unique serial code and signature is required.

- Financial credit notes must be retained for 72 months after filing the annual return to ensure compliance and prevent duplicate claims.

All GST-registered individuals have to issue tax invoices. If any situations occur during the business that cause a reduction in the taxable supply value, the supplier can initiate a credit memo or credit note issuance. Here, we have discussed the typical intricacies of a financial credit note under GST.

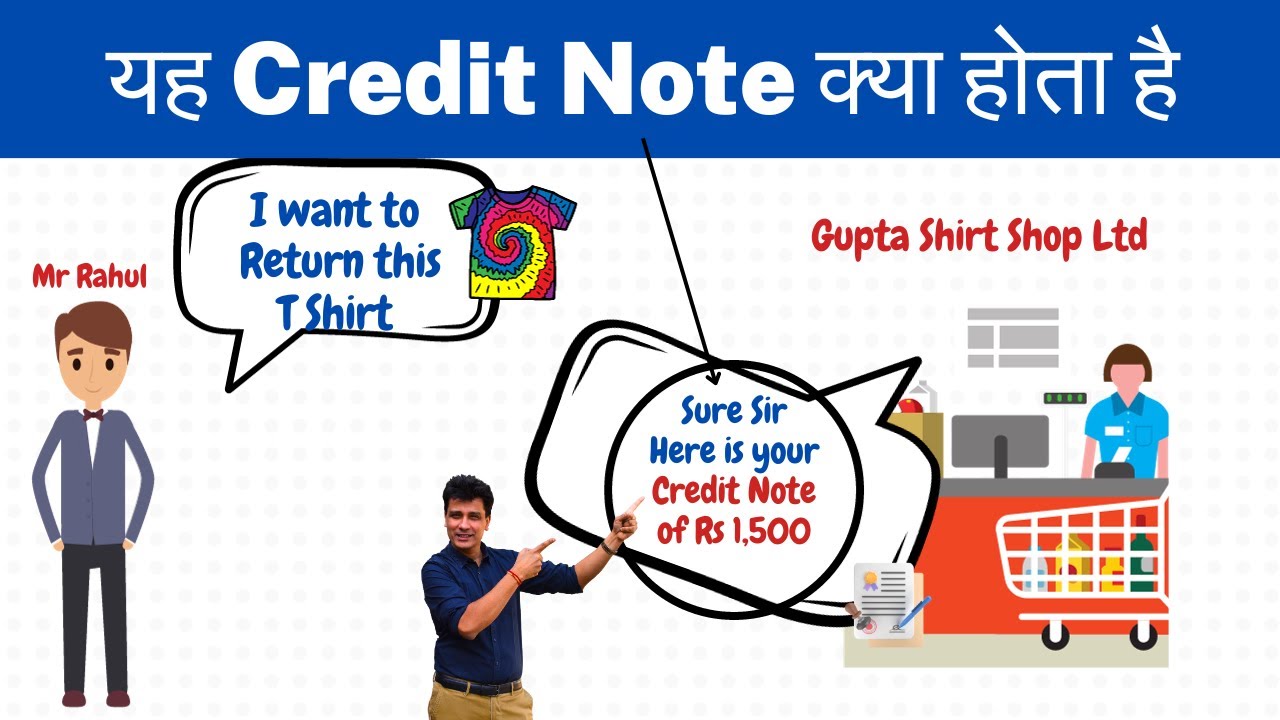

What Is a Financial Credit Note?

A financial credit note is very common and is issued by all types of businesses. Suppliers, who particularly wish to credit the accounts of their customers for different reasons, issue this document. The cause of permitting a credit can be a discount, damage while shipping, cost distinction, etc.

When to Issue a Financial Credit Note?

As per the GST statute, individual credit notes can be issued during the following instances:

- The tax levied in the tax invoice includes additional charges other than the applicable tax for the delivered supplies

- In cases where the services or goods involved are discovered to be insufficient

- Taxable value seems to exceed the estimated taxable sum which was previously supposed to be imposed

- In situations when the customer returns any goods or wants refunds for services

Must reads

Key Details of Credit Notes

There is no prescribed credit note format as per the GST Act. However, the concerned supplier has to ensure the credit note matches the following data:

- Business name, location of supply supply type and GSTIN of the supplier

- Category of the document (it can either be a debit note or a credit note)

- The date on which the document is being issued

- A unique 16-character serial code. The issuer can prefer to keep this serial number as numeric, alphabetic or alphanumeric (including special characters is also allowed)

- The rate of tax and GST value of the supply along with the taxable amount credited to the customer

- Signature of the authorised supplier or his relevant representative's signature

Following the nuances of credit notes is essential for filing a valid tax refund.

💡 If you want to pay your GST with Credit Card, then download Pice Business Payment App. Pice is the one stop app for all paying all your business expenses.

Impact of Financial Credit Notes on GST Returns

The necessity to file financial credit notes has helped streamline the regular tax return filing process. For any business, now it is important to generate debit/ credit notes to maintain transparency on both ends. The credit-debit notes relevant to GST norms must be duly reported while filing quarterly/ monthly returns.

The issue of credit note proves to be useful for both sellers and customers. If you are unsure about the advantages of the issuance of credit note, here we have listed a few of them:

- Credit notes help rectify discrepancies in billing

- It provides formal documentation for returned supplies

- Suppliers can successfully maintain account reconciliation

- Vendors issue credit notes to easily settle disputes surrounding product quality or overpricing

- Easy adjustments to GST liability with credit notes become possible

Overall, these documents assist business persons in resolving disputes that may arise while filing returns. Maintaining proper GST credit notes is highly advised for uninterrupted business operations.

Procedure for Issuing a Tax Credit Note

We suggest you go through the below-mentioned example to understand the process of issuing a financial credit note:

Stage 1: Supplier A sells taxable B2C supplies to one of their clients, accompanied by original invoices.

Stage 2: The client identified quality discrepancies in the end product and initiated a return to supplier A with a corresponding debit note.

Stage 3: Supplier A acknowledges receipt of the debit note and will subsequently issue a credit note to document the returned commodities.

No set time limit has been stipulated for the issuance of a debit or credit note. Both debit and credit notes issued during a given month must be declared in the corresponding GST return.

Nevertheless, the GST portal mentions a particular time limit within which these documents can be declared by tax professionals for a particular financial year. A supplier can declare them on earlier of the below-mentioned dates:

- 30th September of the year following the tax period during which the concerned supply was made

- Actual date of filing the yearly return pertaining to the concerned period

Must reads

The Bottom Line

To ensure direct tax compliance, any financial credit note under GST must be retained for a minimum of 72 months following the filing of the corresponding annual return. It allows a registered person to claim a reduction in tax liabilities legally. In addition, it aids authorities in readily identifying instances of claim duplication by individuals who attempt to unlawfully reduce their output GST liability.

FAQs

What is meant by financial credit note?

A financial credit note is a document issued by a supplier to the buyer to reduce the taxable value of a supply due to reasons like discounts, product returns, or billing discrepancies. It serves to correct the previously issued invoice by adjusting the tax liability and the amount due from the buyer.

Is GST charged on financial credit notes?

GST is not charged on a financial credit note itself. Instead, the issuance of a credit note reduces the taxable value of the original transaction, leading to a corresponding adjustment in the GST amount, reducing the supplier's output tax liability.

What is the treatment of a credit note in GST?

In GST, a credit note reduces the taxable value and, consequently, the GST liability of the supplier. The supplier must report the credit note in their GST return for the relevant period to adjust the tax liability. The buyer's input tax credit is also affected based on the adjustment.

What is a financial debit note under GST?

A financial debit note under GST is issued by a supplier when there is an increase in the taxable value of a supply. This could occur due to undercharged goods or services in the original invoice, and it leads to an increase in the supplier's GST liability.

What is the difference between debit note and credit note?

A debit note is issued to increase the taxable value, often when additional charges are incurred or goods are undercharged. A credit note, on the other hand, reduces the taxable value, usually due to returned goods, discounts, or overcharges. Both documents adjust the original invoice and affect the tax liability.

What is the time limit for credit note under GST?

A credit note under GST must be reported before the earlier of two dates: either by 30th September of the year following the financial year in which the original supply was made or the date of filing the annual return for that year.

What is an example of a credit note?

An example of a credit note is when a supplier issues an invoice for ₹1,000 worth of goods, but the buyer returns goods worth ₹200 due to defects. The supplier issues a credit note for ₹200 to adjust the taxable value and reduce the amount owed.

Why is a credit note called a credit note?

A credit note is called so because it credits the buyer’s account, reducing the amount they owe to the supplier. It acts as formal documentation of a reduction in the buyer's liability, either due to returned goods or billing adjustments.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction