Step-by-Step Guide for RCM Entry in GSTR 3B

Bio

Sandipan Mitra is the CEO and co-founder of Pice. He boasts eight years of experience in the B2B and fintech sector. Sandipan's journey includes significant roles at multiple Indian Unicorns Including Product at PayU, and as founding member / VP, Product at Open Financial Technologies.

- 22 Aug 24

- 12 mins

Share

Step-by-Step Guide for RCM Entry in GSTR 3B

- 08 Mins

- 22-08-24

Table of Contents

- What is the Reverse Charge Mechanism (RCM) under GST?

- RCM and Registered Persons

- What is the Meaning of RCM Return in GST?

- Eligible Input Tax Credit and Input Credit Reversal

- How to show RCM on a GST return?

- Reporting of RCM Transactions in Various GST Returns by the Supplier

- Is There a Provision for Input Tax Credit under the Reverse Charge Mechanism?

Share

Key Takeaways

- Reverse Charge Mechanism: RCM shifts GST liability from the supplier to the recipient, ensuring tax compliance in specific scenarios.

- Recipient's GST Responsibility: Under RCM, recipients must calculate, pay, and report GST directly to the government.

- Claiming ITC: Recipients can claim input tax credit (ITC) on GST paid under RCM for business-related goods and services.

- Accurate GSTR Reporting: Properly report RCM transactions in GSTR-1 and GSTR-3B to maintain compliance and facilitate ITC claims.

- Timely GST Payments: Ensure timely payment of GST and meticulous documentation to avoid penalties and ensure smooth tax operations.

The complexities of the Goods and Services Tax (GST) in India can be challenging, especially when dealing with the Reverse Charge Mechanism (RCM). RCM is a crucial component of GST that ensures tax compliance in specific situations. In this article, we'll explore how to file RCM in GST returns, understand its meaning, and the steps involved in reporting it for both suppliers and recipients.

Handle all your sales and purchase invoices in one place.

Pice’s all-in-one invoice management tool helps you track, send, and organize invoices from a single dashboard. Automatically share new invoices with customers, send timely payment reminders, and keep your collections under control—effortlessly.

Want early access? Fill out this form to get request a demo!

What is the Reverse Charge Mechanism (RCM) under GST?

The Reverse Charge Mechanism (RCM) under GST is a pivotal concept within the Goods and Services Tax (GST) framework in India. It significantly alters the traditional approach to tax liability, particularly focusing on taxable supplies and registered persons. Here’s an in-depth look at RCM and its implications.

Reverse Charge Mechanism (RCM)

The Reverse Charge Mechanism is a system where the responsibility to pay GST shifts from the supplier to the recipient of goods or services. This shift ensures better tax compliance and collection, especially in sectors involving unregistered persons or dealers. Under RCM, the recipient is liable to pay the tax directly to the government, rather than the supplier collecting and remitting it.

Key Situations Where RCM Applies

- Taxable Supplies from Unregistered Dealers: When a registered person purchases goods or services from an unregistered dealer, RCM comes into play. The registered person must pay the GST on these supplies.

- Specific Notified Goods and Services: Regardless of the supplier's registration status, the government specifically notifies certain goods and services to fall under RCM. Examples include cashew nuts, legal services, and import of services.

- Import of Services: When services are imported, the recipient in India must pay GST under RCM, ensuring that supply of services consumed within the country is taxed appropriately.

RCM and Registered Persons

Registered persons under GST must be vigilant about their transactions with unregistered suppliers. They need to identify RCM-business liable transactions, calculate the GST taxes payable, and ensure timely payment to the government. This mechanism helps the government capture tax from transactions that might otherwise fall through the cracks.

Impact on Input Credit

Under the RCM, the recipient who pays the GST can claim Input Tax Credit (ITC) on the tax paid, provided the goods or services are used for business purposes. This process involves:

- Claiming ITC: Once the GST is paid under RCM, the recipient can claim ITC, reducing their overall tax liability.

- Debit and Credit Notes: Adjustments for RCM transactions often involve issuing debit or credit notes, ensuring accurate tax records and compliance.

Compliance and Reporting

To ensure compliance with RCM provisions, recipients must report RCM transactions in their GST returns. This involves:

- Accurate Reporting: Transactions liable for RCM should be meticulously reported in the GST returns to avoid penalties.

- Time of Supply: Determining the time of supply is crucial for RCM, as it dictates the due date for GST payment.

- Non-GST Outward Supplies: RCM transactions must be distinguished from non-GST outward supplies to ensure accuracy in reporting.

GST Rates and Non-Taxable Territory

RCM transactions are subject to specific GST rates, which must be adhered to during tax calculation and payment. Additionally, understanding the distinction between taxable and non-taxable territory tax helps in accurate reporting and compliance.

What is the Meaning of RCM Return in GST?

An RCM return in GST refers to the business process and documentation involved in reporting transactions where the recipient, rather than the supplier, is liable to pay GST. This is crucial for ensuring that all taxable supplies are accurately accounted for, especially those involving unregistered persons or suppliers.

Key Elements of RCM Return

- Unregistered Person: When goods or services are procured from an unregistered person, the registered recipient must pay the GST under RCM. This includes reporting the transaction in their GST return.

- Debit Notes: Adjustments and corrections in RCM transactions may require the issuance of debit notes. These notes help in aligning the taxable value and GST liability accurately.

- Reverse Charge Basis: The core principle of RCM is the reverse charge basis, where the recipient assumes the tax responsibility. This mechanism ensures that GST is collected efficiently, even from sectors with unregistered suppliers.

- GST Liability: Under RCM, the GST liability shifts to the recipient, who must calculate and remit the tax directly to the government. This requires meticulous tracking and reporting in the GST return.

- Taxable Person: In the context of RCM, the taxable person is the recipient of goods or services who must comply with GST regulations by paying the rate of tax and filing the RCM return.

- E-Commerce Operators: E-commerce operators also fall under RCM for specific transactions, where they are required to collect and pay GST on behalf of the suppliers.

Eligible Input Tax Credit and Input Credit Reversal

Under RCM, the recipient who pays the GST is eligible for Input Tax Credit (ITC) on the tax paid, provided the goods or services are used for business purposes. However, if the conditions for ITC are not met, input credit reversal may be necessary, which should be reported accurately in the GST return.

Reporting and Compliance

Accurate reporting and compliance are essential in RCM returns to avoid penalties and ensure seamless tax administration. This involves:

- Time of Supply: Determining the time of supply is critical for RCM transactions as it dictates the due date for GST payment and reporting.

- Zero-Rated Supplies and Applicable Rate: Understanding the applicable GST rate and distinguishing zero-rated supplies help in accurate reporting and compliance.

- ERP and E-TDS Return Filing Solution: Leveraging ERP systems and E-TDS solutions can streamline the process of filing RCM returns, ensuring accurate and timely submissions.

- Vendor Payments and Payment Vouchers: Proper documentation, including payment vouchers and vendor payments, supports the accurate reporting of RCM transactions.

- Invoice Level Reporting: Detailed reporting at the invoice level ensures transparency and compliance with GST regulations.

Business Compliance and Composition Dealer

Businesses must adhere to compliance requirements under RCM, including the accurate filing of returns and payment of GST. Composition dealers, although typically dealing with lower compliance requirements, must also understand their responsibilities under RCM.

How to show RCM on a GST return?

General Guidelines

- Identify RCM Transactions: Recognize which transactions are liable for RCM.

- Calculate GST Payable: Compute the GST amount due on these transactions.

- Report Transactions: Enter details in the appropriate sections of your GST returns.

- Pay GST: Ensure the GST due under RCM is paid directly to the government.

- Claim Input Tax Credit (ITC): If eligible, claim ITC on the GST paid.

Must reads

Reporting of RCM Transactions in Various GST Returns by the Supplier

Steps to Show RCM in Various GST Returns

GSTR-1 (Outward Supplies)

GSTR-1 is a monthly or quarterly return detailing all outward supplies of goods and services. For RCM transactions:

- Section for Outward Supplies Liable to Reverse Charge:

- Enter the details of all supplies subject to RCM, including the GSTIN of the recipient, the taxable value, and the tax amount.

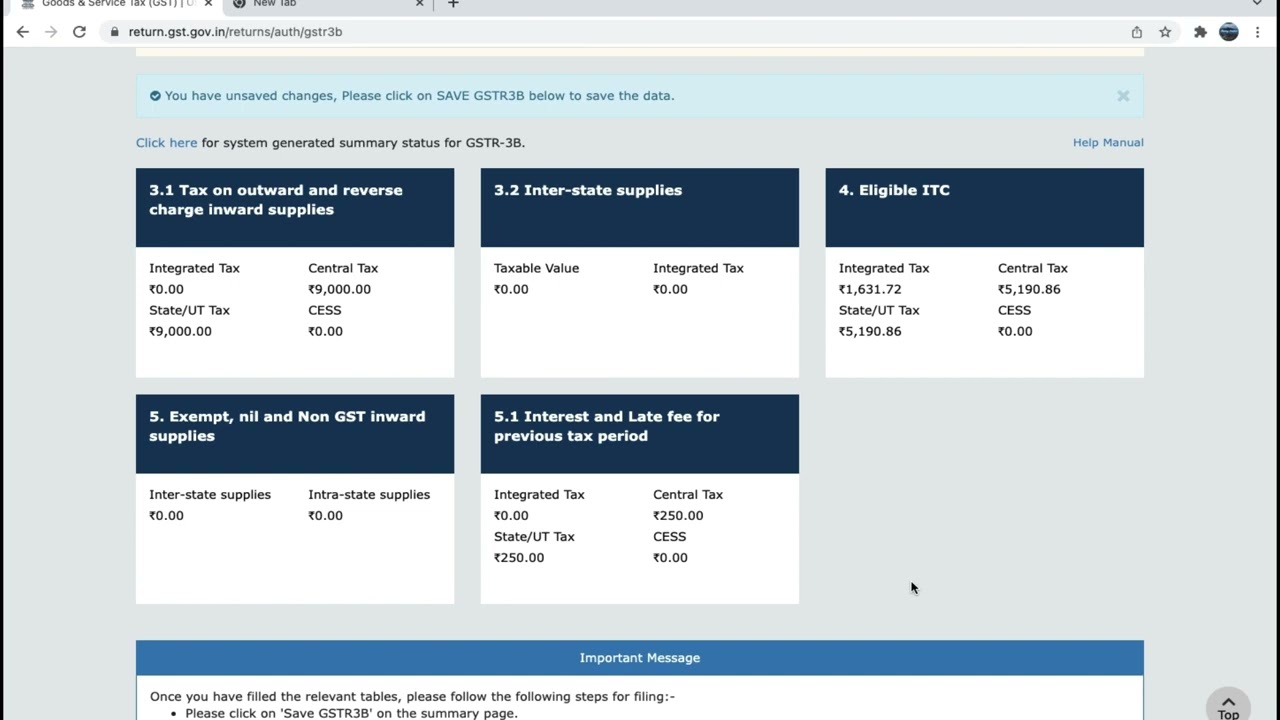

GSTR-3B (Monthly Summary Return)

GSTR-3B is a summary return of all inward and outward supplies, including RCM transactions:

- Section 3.1 (Tax on Outward and Reverse Charge Inward Supplies):

- Enter the taxable value and tax amount under "3.1(d) - Inward supplies (liable to reverse charge)".

- Section 4 (Eligible ITC):

- Claim the input tax credit (ITC) on RCM if eligible.

GSTR-9 (Annual Return)

GSTR-9 is the annual return that consolidates all transactions for the financial year:

- Table 4 (Details of Advances, Inward and Outward Supplies):

- Report the total taxable value and tax amount of outward supplies liable to reverse charge in Table 4.

- Table 6 (Input Tax Credit):

- Report the ITC claimed on RCM transactions in Table 6.

- Table 7 (Reconciliation of ITC):

- Reconcile the ITC on inward supplies liable to reverse charge.

Reporting of RCM Transactions in Various GST Returns by the Recipient

Reporting of RCM Transactions in GSTR-2B

GSTR-2B is a static statement that shows the recipient's ITC:

- Inward Supplies Section:

- Report the details of inward supplies liable to a reverse charge.

- Ensure the accuracy of the reported data to claim ITC.

Is There a Provision for Input Tax Credit under the Reverse Charge Mechanism?

Yes, there is a provision for Input Tax Credit (ITC) under RCM. The recipient can claim ITC on the GST paid under RCM, provided the goods or services are used for business purposes. Proper documentation and timely reporting are crucial for availing ITC benefits.

An Input Service Distributor (ISD) is a regular taxpayer registered under GST to distribute the Input Tax Credit (ITC) of goods and services received to its branches or units. The role of an ISD is crucial in maintaining proper tax credit distribution across different business units.

Receiving Supplies Liable for RCM

When an ISD receives a supply liable for RCM, several steps must be followed to ensure compliance and proper credit distribution.

Reverse Charge Applicability

The first step is determining the applicability of reverse charge on the received supply. This includes:

- Charge Calculation: Calculating the GST payable under RCM based on the applicable GST rate.

- Charge Entry: Ensuring that the charge is accurately entered in the GST portal to reflect the regular tax liability.

Charges Against Services and Goods

The reverse charge can apply to both services and goods. The ISD must:

- Identify the Supply Type: Determine if the supply is a service or good, as reverse charge provisions may differ.

- Charge Applicable: Apply the correct GST rate details for the specific type of supply.

Steps for an ISD When Receiving RCM Supplies

Step 1: Payment of GST: The ISD must pay the GST on the supply received under RCM. This is done by calculating the tax and making the payment to the government.

Step 2: Credit Distribution: After paying the GST, the ISD can distribute the input tax credit (ITC) to the respective branches or units. This involves:

- Credit Relates: Ensuring the ITC relates to the business operations of the units receiving the credit.

- Credit Under Clause: Distributing the ITC under the relevant GST clauses and provisions to ensure compliance.

Step 3: Documentation and Reporting: Proper documentation is essential. The ISD must maintain records of the received supply, GST payment, and ITC distribution.

- Charge in GST Portal: Enter the transaction details accurately in the GST portal.

- Reverse Charge Provisions: Follow the reverse charge provisions strictly to avoid penalties and ensure compliance.

What Happens When an Input Service Distributor Receives a Supply Liable for Reverse Charge Mechanism under GST?

When an input service distributor (ISD) receives a supply liable for RCM:

- Reporting: The ISD must report the RCM transaction in their GST returns.

- Distribution of ITC: The ITC on such supplies should be distributed to the respective units based on the rules prescribed under GST.

- Documentation: Maintain proper documentation to support the distribution of ITC.

Conclusion

Filing RCM on GST returns involves meticulous reporting and compliance. Understanding the steps to report RCM in GSTR-1, GSTR-3B, GSTR-9, and GSTR-2B is crucial for both suppliers and recipients. Properly managing RCM ensures that businesses remain compliant with GST regulations and can effectively claim ITC.

💡Learn more about how our Pice can help you make all your important business payments, like supplier and vendor payments, rent, GST, & utility, from one single dashboard with your credit card. Request a demo now.

FAQs

How to Reverse Charge Mechanism Transactions in GST Returns?

To report Reverse Charge Mechanism (RCM) transactions in GST returns, the recipient must identify all transactions liable for RCM and calculate the GST payable. These transactions are then reported in specific sections of the GST returns, such as GSTR-3B and GSTR-1. Accurate documentation and timely payment of the GST due are crucial. The recipient must also ensure that input tax credit (ITC) claims are accurately reported, if applicable.

Under RCM, who is responsible for paying GST?

Under the Reverse Charge Mechanism (RCM), the responsibility for paying GST shifts from the supplier to the recipient of goods or services. This means the recipient must calculate and remit the GST directly to the government, rather than the supplier collecting and paying it. This mechanism is designed to ensure tax compliance and efficient collection from sectors where the supplier may be unregistered or operate informally.

How to file an RCM in a GST return?

To file RCM in GST returns, the recipient must first identify all RCM-liable transactions. The GST payable on these transactions is calculated and reported in the appropriate sections of the GST returns, such as GSTR-3B and GSTR-1. The recipient must pay the GST directly to the government and can claim Input Tax Credit (ITC) if eligible. Proper documentation and accurate reporting are essential to ensuring compliance.

Is There a Provision for Input Tax Credit under the Reverse Charge Mechanism?

Yes, there is a provision for Input Tax Credit (ITC) under the Reverse Charge Mechanism (RCM). The recipient who pays GST under RCM can claim ITC, provided the goods or services are used for business purposes. The ITC can be claimed in the GST return by reporting it in the relevant sections, ensuring that all conditions for claiming ITC are met and proper documentation is maintained.

How to Show RCM Sales in GSTR Filing?

To show RCM sales in GSTR filing, the recipient must report the details of such transactions in the appropriate sections of GSTR-1 and GSTR-3B. In GSTR-1, RCM transactions are reported under the outward supplies liable to reverse charge section. In GSTR-3B, they are included under the inward supplies liable to reverse charge section. Accurate reporting ensures compliance and facilitates the correct calculation of GST liability and Input Tax Credit (ITC) claims.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction