Table 4 of GSTR-3B – New Changes to Format, Reporting Procedure, Impact on Taxpayers

Bio

Ankit Rahangdale is a seasoned finance professional with a distinguished background as a Chartered Accountant. Currently, he leads the Finance Department at Pice. With over five years of invaluable experience in the banking and finance sector, honing his expertise through esteemed institutions such as ICICI Bank and Standard Chartered Bank.

- 26 Aug 24

- 11 mins

Share

Table 4 of GSTR-3B – New Changes to Format, Reporting Procedure, Impact on Taxpayers

- 08 Mins

- 26-08-24

Table of Contents

- Contents of Table 4 of GSTR-3B and Applicability

- GSTR-3B Format

- GSTR-3B Due Date

- Old Format of Table 4 of GSTR-3B

- New Format of Table 4 of GSTR-3B

- What Is the Procedure to be Followed by Taxpayers While Filing Their GSTR-3B?

- Why Is Ineligible ITC Under Section 17(5) Now Reported in Table 4(B) and Not Table 4(D)?

- Conclusion

Share

Key Takeaways

- Detailed ITC Reporting: The new Table 4 format in GSTR-3B, effective from August 2022, requires a precise breakdown of Input Tax Credits (ITCs), including reversed, restricted, and eligible credits.

- Auto-population: Table 4(A) auto-populates from GSTR-2B, requiring taxpayers to separate eligible and ineligible ITCs, improving accuracy and reducing manual errors.

- Reversal Tracking: Taxpayers must report non-reclaimable ITC reversals in Table 4(B)(1) and reclaimable reversals in Table 4(B)(2), ensuring compliance with GST rules.

- Accurate Tax Liability: Proper reporting of ITC impacts the net ITC balance, ensuring accurate tax liability and preventing penalties or notices.

- Streamlined Audits: Continuous tracking and integration of transactions into GSTR-2B improve control for auditing firms, simplifying the verification of ITC claims.

Starting in July 2022, taxpayers have reported specific modifications when filing the GSTR-3B return. These modifications have brought about a fresh approach to presenting data in Tables 3 and 4 of the form.

The first time, this revision came to public discussion via Notification No. 14/2022 – Central Tax. Later on, by September, the GSTN published the new format for conveying data in Table 4 of GSTR-3B.

The new format has accommodated a more detailed split of Input Tax Credits (ITCs), explaining which are reversed, restricted, reclaimed, eligible and so on. In this blog, you will get the ultimate checklist of the new modifications made in Table 4 and consequently, how taxpayers need to make adjustments moving forward.

Contents of Table 4 of GSTR-3B and Applicability

The updated format for Table 4 of Form GSTR-3B Return was implemented for the first time in August 2022. To comply with GSTR-3B, one must provide a comprehensive breakdown of ITC details in Table 4 for a specific return period. These details include ITC imposed on capital goods, goods and services import, inward supplies that are subjected to reverse charge, etc.

Information like ITC reversals and ineligible ITC are also declared in Table 4. It is necessary to correctly summarize the ITC as it determines the GST liability towards the government. Incorrect reporting can lead to notice issuance or even penalties.

GSTR-3B Format

Here is the format of Form GSTR-3B:

First, when you are about to file the return, you will be prompted to enter your GST number. Next, you will notice your name getting auto-populated in the consequent field.

3.1 – Details of Outward Supplies and Inward Supplies Liable to Reverse Charge (Other Than Those Covered by Table 3.1.1)

After a couple of initial entries, you will find Section 3.1, outlining specifications of outward and inward supplies liable to reverse charge. These details have been listed as follows:

- 3.1(a) - Outward taxable supplies (other than zero rated, nil rated and exempted) = related to State and Central Sales along with the applicable GST amount.

- 3.1(b) - Includes outward supplies that are made towards SEZ. These are supplies with zero GST rate.

- 3.1(c) - Outward supplies that are nil-rated and exempt like milk, sugar, etc.

- 3.1(d) - Inward supplies liable to reverse charge or simply purchases made from unauthorised sellers for which you need to make an invoice yourself

- 3.1(e) - Non-GST outward supplies or goods that are not covered under GST like alcohol, petroleum products, etc.

3.1.1– Details of Supplies Notified Under Sub-section 9(5) of the Central Goods and Services Tax Act, 2017 and Corresponding Provisions in Integrated Goods and Services Tax/Union Territory Goods and Services Tax/State Goods and Services Tax Acts.

As you come down to 3.1.1, it enlists supplies published under Sub-section 9(5) of the Central Goods and Services Tax Act, 2017. In addition, it mentions the corresponding provisions of the Integrated Goods and Services Tax/Union Territory Goods and Services Tax/State Goods and Services Tax Acts.

Under 3.1.1, you will find the following supplies:

- Taxable supplies on which e-commerce operators furnish tax under Sub-section (5) of Section 9.

- Taxable supplies manufactured by a registered entity via an e-commerce operator, on which the tax has to be paid by the operator as per sub-section (5) of section 9.

3.2 – Out of Supplies Made in 3.1(a) and 3.1.1 (i), Details of Inter-State Supplies Made

Continuing further, you will come down to 3.2 which encapsulates details of inter-state supplies, out of supplies made in 3.1(a) and 3.1.1 (i).

Here are the nature of supplies mentioned in 3.2:

- Supplies made to Unregistered Persons

- Supplies made to Composition Taxable Persons

- Supplies towards UIN Holders

4. Eligible ITC

This section is further divided into 4(A), 4(B), 4(C) and 4(D). Here’s the complete breakdown:

- 4(A) – ITC Available (Whether in Full or Part)

Under 4(A), there are 5 components:

- i) Tax charged on import of commodities

- ii) Tax paid on import of services that come under Reverse Charge

iii) Inward supplies that are liable to Reverse Charge

- iv) Inward supplies via your Input Service Distributor (ISD)

- v) All other ITC (any purchase made from a registered dealer)

- 4(B) - ITC Reversed

(1) - The first row mentions - As per rules 38 42 & 43 of CGST Rules and section 17 (5):

These rules call for the reversion of input credit, some of which were used for business and the rest for other purposes. As a matter of fact, input credit reversal also becomes crucial where supplies are nil-rated or exempt from tax.

(2) - Others = these are the supplies that have been reversed in your books

- 4(C) Net ITC Available

This section calculates the Net of Available – Reversed ITC

- 4(D) - Other Details

Here, you have to address two parts:

- ITC reclaimed which was reversed under Table 4(B)(2) in earlier tax period

- Ineligible ITC under section 16(4) & ITC restricted due to PoS rules

5 - Values of Exempt, Nil-Rated and Non-GST Inward Supplies

Section 5 involves all the values of exempt, nil-rated and non-GST inward supplies. It covers supplies via a dealer who is under the composition scheme, including inter-state and intra-state supply of goods. Additionally, you find non-GST supplies.

6 - Payment of Tax

It is the final segment that clarifies the amount of tax payable to the government. The final sum is separately mentioned under IGST, CGST, SGST and UTGST.

A taxpayer needs to file the credit availed against the aforementioned sections. To find the amount, one must refer to 4(C). If there is a late fee deposited with the tax sum that needs to be reported explicitly.

GSTR-3B Due Date

GSTR-3B is a monthly self-declared summary GST return that is due on the 20th of the following month. For instance, if we are considering the due date of GSTR 3B for May 2024, then it would be due before 20th June 2024. It is crucial to note down the return filing due dates to avoid penalties on GST returns.

Old Format of Table 4 of GSTR-3B

In the old format of Table 4 of GSTR-3B, taxpayers were required to report all available Input Tax Credits (ITCs) in Table 4(A). Previously, this table became auto-populated through the GSTR-2B. Moreover, it excluded the ineligible ITC.

Additionally, the taxpayers reported all Input Credit Tax that got reversed according to Rules 42 and 43 of the CGST Rules in Table 4(B).

- Rule 42 limits ITC availability for supplies that are partially used in commercial aspects and exempt supplies.

- Rule 43 limits ITC on capital goods by applying a similar set of reasons. The taxpayers could refer to the net claimable ITC in Table 4(C).

Eventually, you had to report ineligible ITC such as goods/services used for personal purposes, motor vehicles, specific insurance premiums, etc., in Table 4(D).

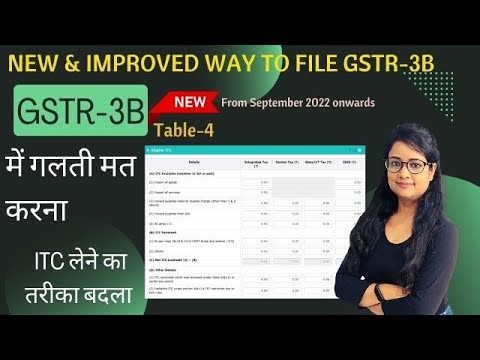

New Format of Table 4 of GSTR-3B

?feature=shared

?feature=shared

The new format of Table 4 of GSTR 3B Return Form that came into force in August 2022 has 4 different sections - 4(A), 4(B), 4(C) and 4(D) respectively.

In every tax period, Table 4(A) gets auto-populated, deriving the requisite information from the GSTR-2B statement. However, you need to bifurcate the ITC into ineligible and eligible before filing the GSTR-3B report.

In the next stage, the bifurcation of ineligible ITCs takes place into permanent and temporary reversals. Temporary reversals are simply the ITC which you may reclaim at a later date.

In Table 4(B)(1), you have to report all non-reclaimable reversals of input tax credit. These include reversals as per:

- Rule 38 of the CGST Rules - these limitations apply only to banking organisations.

- Rule 42 and 43 of the CGST Rules - these ITC restrictions apply to supplies that are partly used for business purposes.

- Section 17(5) of the CGST Act - represents the ineligible ITCs that were previously mentioned in Table 4(D) of the old format.

Coming next is Table 4(B)(2), where you must report all reclaimable reversals. Here you report ITC that falls under:

- Rule 37 of the CGST Rules - unsettled transactions within the previous 180 days

- Section 16(2)(b) of the CGST Act - applies to invoices where the goods/services have not yet been received

- Section 16(2)(c) of the CGST Act - here the suppliers are yet to clear their GST dues

- Auto-populated credit notes

Upon mentioning all the above details, you will see the net ITC which is 4(A) - 4(B) in 4(C).

Finally, you reach 4(D) where there are two more subparts 4(D)(1) and 4(D)(2). The latter half must be accessed to report ITCs that are not available by law. An example of such a transaction can be CGST/SGST paid during a hotel stay in another state. This ITC gets restricted because of place of supply (PoS) regulations.

What Is the Procedure to be Followed by Taxpayers While Filing Their GSTR-3B?

Here's a detailed procedure for taxpayers to follow while filing their GSTR-3B:

Here's a detailed procedure for taxpayers to follow while filing their GSTR-3B:

- Except for the ITC excluded under Section 16(4) or POS rules, the remaining ITC (both eligible and ineligible) gets auto-populated in Table 4(A).

- You have to report the non-reclaimable reversals of ITC in 4(B)(1).

- Next, you must report the temporary or reclaimable reversals in Table 4(B)(2). If you reclaim any of the supplies in future then the same needs to be mentioned under Table 4(A)(5) on meeting certain conditions.

- Additionally, you need to report all the reclaimed ITC in Table 4(D)(1).

- You must check your net ITC in Table 4(C). The same information also gets inscribed in your personal Electronic Credit Ledger.

Please note that there is no need to report ITC that comes under Section 16(4) or POS rules in Table 4(D)(2).

Why Is Ineligible ITC Under Section 17(5) Now Reported in Table 4(B) and Not Table 4(D)?

After revising the format of Table 4, the data in Table 4(A) is automatically carried forward from the GSTR-2B along with ineligible ITC. The ineligible ITC, if not properly bifurcated and reversed in Table 4(B), will instead build up in the net ITC balance of the registered person. This will be a wrong assessment of net payable tax.

The objective of the government is to make sure that taxpayers declare the correct value of ineligible ITC and eligible ITC. It assists them in comparing the figures filed in GSTR-3B with GSTR-2B and GSTR-9 with GSTR-3B.

How Does This Change Impact Taxpayers?

The new Table 4 format in GSTR-3B requires stricter tracking of ITC. Taxpayers must now report ineligible ITC and separate reversals (reclaimable vs non-reclaimable) impacting tax liability. While this introduces more complexity, it enhances tax administration and reduces errors in GST reporting.

Conclusion

All the new modifications in Table 4 of GSTR-3B have now made it necessary for taxpayers to include a dedicated section in their financial records. This segment must justify all the Input Tax Credits that they cannot claim.

Moreover, the recent updates allow for continuous monitoring of every purchase transaction within the Purchase Register. This data is then automatically integrated into the GSTR-2B report. Consequently, it has given the ultimate control to auditing firms, making their job easier.

💡Facing delays in GST payment? Get started with PICE today and streamline your GST payments. Click here to sign up and take the first step towards hassle-free GST management.

FAQs

What are the key changes in the new Table 4 format of GSTR-3B?

The new format requires a detailed breakdown of Input Tax Credits (ITCs), including categories for reversed, restricted, and eligible credits, and mandates stricter reporting for non-reclaimable and reclaimable ITC reversals.

How does the auto-population of Table 4(A) from GSTR-2B affect taxpayers?

The auto-population simplifies the filing process by reducing manual entry errors but requires taxpayers to correctly bifurcate eligible and ineligible ITCs before submission.

What should taxpayers report under Table 4(B)(1) and 4(B)(2)?

Table 4(B)(1) is for non-reclaimable ITC reversals, while Table 4(B)(2) is for reclaimable ITC reversals, ensuring accurate adjustments and compliance with GST rules.

How does accurate ITC reporting impact tax liability?

Proper reporting of eligible and ineligible ITCs and ITC reversals ensures the correct net ITC balance, preventing discrepancies in tax liability and avoiding penalties or notices.

How do the new modifications streamline the auditing process?

Continuous tracking and integration of purchase transactions into GSTR-2B improve control and accuracy, making it easier for auditing firms to verify ITC claims and ensuring compliance.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction