Invoice Matching Under GST

Bio

Sandipan Mitra is the CEO and co-founder of Pice. He boasts eight years of experience in the B2B and fintech sector. Sandipan's journey includes significant roles at multiple Indian Unicorns Including Product at PayU, and as founding member / VP, Product at Open Financial Technologies.

- 18 Nov 24

- 6 mins

Share

Invoice Matching Under GST

- 08 Mins

- 18-11-24

Key Takeaways

- Invoice matching ensures accurate Input Tax Credit (ITC) claims under GST.

- GSTN auto-populates supplier data to simplify reconciliation in GSTR-2A.

- Timely GSTR-2 filing avoids penalties and boosts compliance ratings.

- Only registered taxpayers must file GSTR-2, with specific exemptions.

- Invoice matching strengthens transparency and efficiency in the GST system.

Every month suppliers have to upload their invoices to the GSTN portal, where these will be compared with the customers' purchases. Therefore, invoice matching has become a regular process for businesses. The adoption of IT systems for bookkeeping and tax compliance is expected to increase, even among small and medium businesses.

In well-integrated IT systems, suppliers and buyers will be able to match their invoices well. GST invoice matching plays a vital role in trading activities. In this blog, we will explore what invoice matching under GST is and discuss other essential details.

What Do You Understand by Invoice Matching?

According to the finance minister, “The government can guarantee that eligible input tax credit is correctly allocated between states through the process of invoice matching and the automated GST return mechanism".

Invoice matching is a system where all taxable supplies made under GST are compared with the taxable supplies received by the buyer. The GST Network (GSTN), responsible for developing the IT framework for GST implementation in India, is working diligently to create the algorithms and embed the logic into the GST web application available on the common portal.

Importance of Invoice Matching

The concept of invoice matching is important under the GST law because the input tax credit paid on the purchases of goods or services is allowed only if the particulars filed in the GSTR-2 of the buyer and outward supply details filed in the GSTR-1 of the supplier match. That is done by auto-populating the details of the supplier’s GSTR-1 into the details of the buyer’s GSTR-2.

If the invoicing matching process is not reconciled, the buyer cannot claim input tax credit for the taxes paid on purchased goods or services. Consequently, businesses must adhere to GST compliance rules. Compliance ratings have been introduced to encourage companies to file returns on time and adhere to all relevant regulations.

Must reads

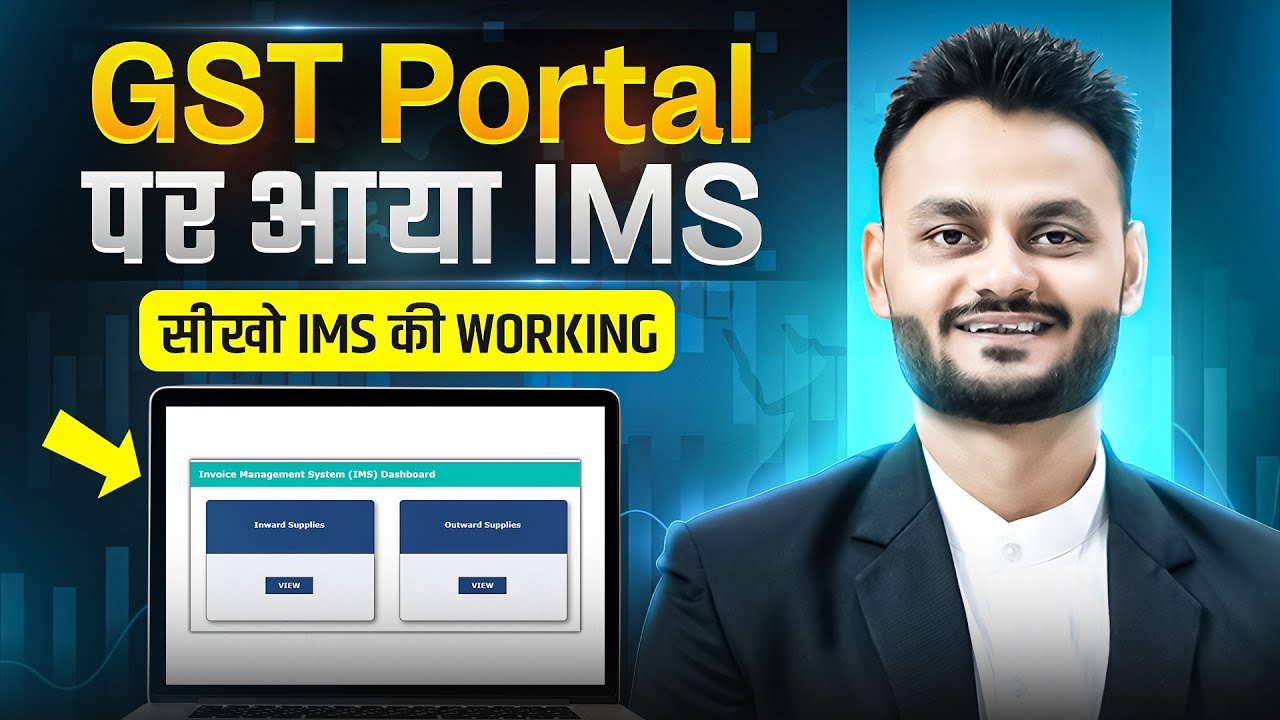

What Is the Process of Invoice Matching?

?feature=shared

?feature=shared

The invoice matching mechanism is crucial because, under GST law, the input tax credit for purchased goods and services can only be claimed if the inward supply details submitted in the buyer's GSTR-2 form match the outward supply details filed in the supplier's GSTR-1.

This connection is established by auto-populating data from the supplier's GSTR-1 into the buyer's GSTR-2. Therefore, if these two records do not align, the buyer will be unable to claim the input tax credit for taxes paid on the purchased goods or services. Compliance ratings serve as an incentive for businesses to file their returns punctually and adhere to related regulations.

Essentially, invoice matching involves reconciling all taxable GST supplies with the taxable supplies received by the buyer. When the supplier submits GSTR-1, the recipient can identify their purchases using the auto-populated GSTR-2A. After making any necessary adjustments, the recipient's electronic credit ledger will be provisionally credited with the input credit.

Any changes or additions made to the GSTR-2 will be reflected in the supplier's GSTR-1A. Once the supplier completes Form GSTR-3 (Monthly Returns Form), the input credit becomes accessible. It is important to consider the tax payments when filling out the monthly returns form. The acceptance of the input tax credit will be indicated in the GST MIS-1 Form.

Claiming Input Tax Credit

A procurer can claim an Input Tax Credit (ITC) as soon as the supplier submits Form GSTR-3. The acknowledgement of the Input Tax Credit must be detailed in Form GST MIS-1.

Components to be Matched

The following are the components that you need to match in the GSTN portal:

- GSTN of the recipient

- GSTN of the supplier

- Invoice or debit note number

- Invoice or debit note date

- Tax amount

- Taxable value

Must reads

What Is the GSTR-2 Form?

The GSTR-2 form is a monthly statement of inward supplies that needs to be submitted by recipient taxpayers. Through this form, they can accept, reject, modify or keep the outward supply details from GSTR-1 as pending. The GSTR-2 return must be submitted regardless of whether any business activity occurred during the specified tax period.

Time-Limit

GSTR-2 for the previous tax period must be submitted by the 15th of each month. Failure to file on time will result in a penalty of ₹100 per day, and without paying this, the taxpayer cannot file GSTR-3.

Conditions for Filing GSTR-2

Certain requirements must be met before submitting form GSTR-2. These include:

- The dealer must be registered under the GST Act and hold an active GSTIN.

- LLPs and companies must have a valid, non-expired digital signature.

- Individuals or entities should have a valid Aadhar number and mobile number to utilise the e-sign option.

Exemptions

The following is the list of individuals who are exempted from filing the GSTR-2 form:

- Taxpayers under the composition scheme.

- Input service distributors.

- Non-resident taxable persons.

Conclusion

Invoice matching under GST is essential for businesses to claim input tax credit. It ensures that the buyer’s inward supplies match the supplier’s outward supplies, helping maintain transparency and accuracy in tax compliance.

By following the proper process and adhering to GST rules, businesses can avoid penalties and ensure smooth transactions. The invoice matching concept not only simplifies tax filing but also strengthens the overall GST system.

💡If you want to streamline your payment and make GST payments, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

What is invoice matching in GST?

Invoice matching is the process of comparing the details of taxable supplies made by a supplier (filed in GSTR-1) with the taxable supplies received by a buyer (filed in GSTR-2). This ensures that the buyer can claim Input Tax Credit (ITC) accurately. The GST Network (GSTN) automates this process through its IT framework.

Why is invoice matching important under GST?

Invoice matching is crucial because ITC is granted only when the buyer’s inward supplies match the supplier’s outward supplies. It prevents discrepancies, ensures transparency, and minimizes tax fraud. Non-compliance can result in penalties and disallowance of ITC claims.

What happens if invoice matching fails?

If invoice matching fails, the buyer cannot claim ITC for taxes paid on purchases. This affects cash flow and compliance ratings. The discrepancies must be rectified by either the buyer or the supplier before filing the returns to avoid penalties or delays.

What are the key components matched during invoice reconciliation?

The key components matched include the GSTIN of the supplier and recipient, invoice/debit note number, invoice/debit note date, taxable value, and tax amount. Any mismatch in these details can disrupt the ITC claim process.

Who is exempt from filing GSTR-2?

Taxpayers under the composition scheme, Input Service Distributors (ISDs), and non-resident taxable persons are exempt from filing GSTR-2. However, other registered taxpayers must file this form to reconcile their inward supplies and claim ITC accurately.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction