Do You Need to Pay GST on Foreign Exchange?

Bio

Sandipan Mitra is the CEO and co-founder of Pice. He boasts eight years of experience in the B2B and fintech sector. Sandipan's journey includes significant roles at multiple Indian Unicorns Including Product at PayU, and as founding member / VP, Product at Open Financial Technologies.

- 3 Oct 24

- 8 mins

Share

Do You Need to Pay GST on Foreign Exchange?

- 08 Mins

- 03-10-24

Key Takeaways

- No GST is applicable on inward remittances as exports are zero-rated supplies.

- GST at 18% applies to foreign currency conversion services based on predefined slabs.

- For foreign exchange involving Indian Rupees, GST is calculated using the RBI reference rate.

- Both-currency foreign exchange transactions are taxed on the lower amount after INR conversion.

- FIRC and BRC services are subject to GST under the reverse charge mechanism.

Understanding the intricacies of Goods and Services Tax is important, especially while dealing with money conversions in the country. Many individuals and businesses need to know the currency exchange value, whether for international trade, foreign investments or travel.

Hence, being aware of the applicability of GST on foreign exchange ensures compliance with tax regulations, and avoids penalties by tax authorities.

In this blog, we will discuss GST for forex transactions, calculations based on various provisions of the CGST Rule and other important aspects.

GST and Foreign Exchange Transactions

Let us find out how GST is applicable to Foreign Exchange Transactions.

1. Inward Remittances to India

GST is not applicable on inward remittances as exports of goods or services are a zero-rated supply. However, there are some online platforms that often charge tax at the rate of 18% on products as a transaction fee in the case of international money transfers. One must note that this fee is not a separate charge for inward remittances.

2. Compliance Handling and Certifications (FIRC & BRC)

Goods and Services Tax is levied on services associated with the issuing of certificates like BRC (Bank Realisation Certificate) and FIRC (Foreign Inward Remittance Certificate). The reverse charge mechanism is applicable here. The liability to pay tax shifts to foreign clients from service providers. Foreign clients pay tax to the Government of India directly, so you are not required to charge tax on the invoice.

3. Foreign Currency Conversion

If you convert the amount you receive in the export of goods or services into Indian rupees, 18% is applicable on the foreign conversion services. Take a look at the slabs below to determine the value in case of sales or purchases of foreign transactions:

Slab 1: Up to ₹1 lakh

If the gross amount is equal to or less than ₹1,00,000, then 1% of the amount is subject to a minimum of ₹250. In this case, the minimum amount of GST to be paid is ₹45.

Slab 2: Ranging Between ₹1 lakh to ₹10 lakh

If the gross amount of foreign currency exchange service ranges between ₹100,00 and ₹10,00,000, then the value of service on which GST is payable is ₹1,000 plus 0.5% of the amount.

Slab 3: More than ₹10 lakh

If the gross amount of foreign currency that has been exchanged is more than the value of ₹10,00,000, then the value of service of which GST is payable is ₹5,500 plus 0.1% of the amount. It is subject to ₹60,000 maximum. In this case, the minimum GST that has to be paid is ₹10,800.

GST on Foreign Exchange Conversion Service in India

When exchanging (buying or selling) foreign currency in India, the value of supply is determined by the service supplier. Generally, there are 2 methods for calculating the value of supply for foreign exchange conversions:

- Calculation Based on Rule 32(2)(a) of CGST Rule, 2017

- Slab Based on Rule 32(2)(b) of CGST Rule 2017

?feature=shared

?feature=shared

Method 1: Calculation Based On Rule 32(2)(a) of CGST Rule, 2017

Under Method 1, let us discuss taxable value calculation based on rule 32(2)(a) of CGST Rule, 2017:

Case 1: When One of the Currencies Being Exchanged Is Indian Currency (INR)

There are two sub-cases:

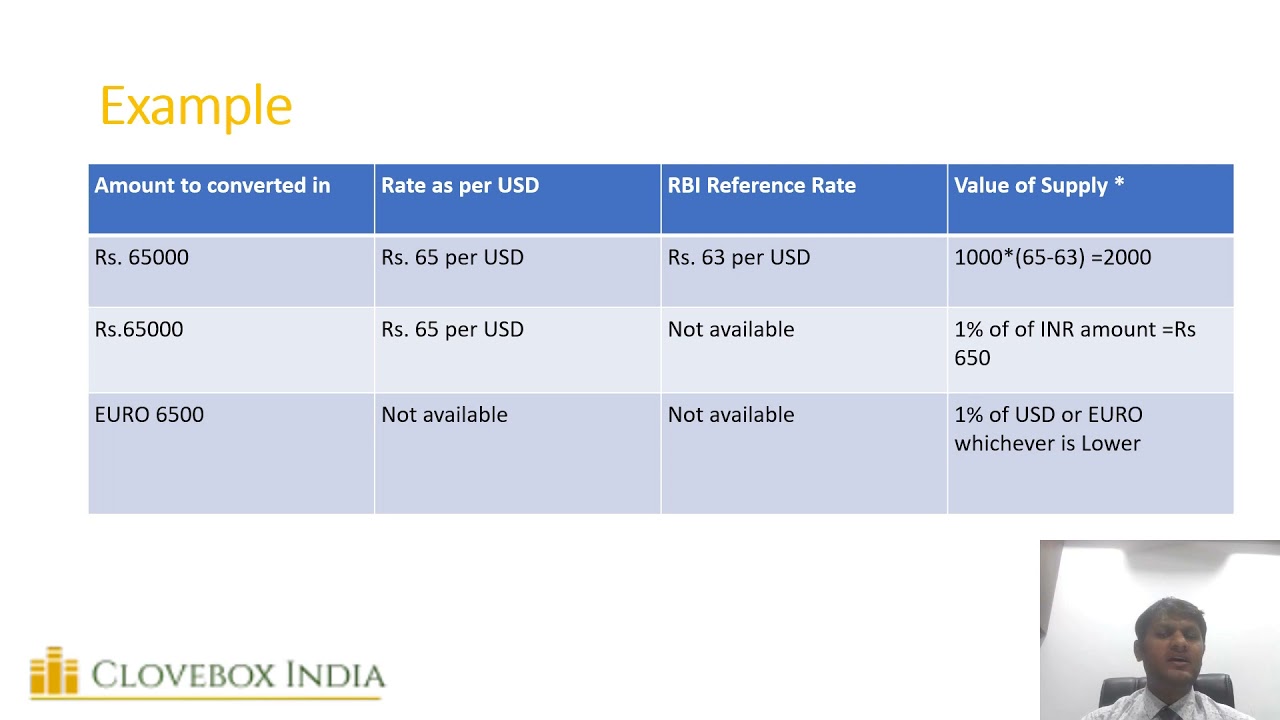

Sub Case No. 1: When the Reserve Bank of India Reference Rate Is Provided

The Reserve Bank of India reference rate decides the value of the difference between two currencies. If the reference rate is provided, the value of foreign currency:

Buying of Foreign Currency: Value = (RBI reference rate – buying rate) * Total currency units

Selling of Foreign Currency: Value= (Selling rate - RBI reference rate) * Total units of currency

Below is an example for better understanding:

Mr. X took Money Exchange's services for conversion of 100 USD to Indian Rupee at the rate of 1 USD is ₹84. The reference rate for USD-INR is, assumingly, ₹83 per USD.

The value of supply (84-83)*100= ₹100.

Therefore, GST on foreign exchange conversion is applicable at the rate of 18%.

Sub Case No. 2: Reserve Bank of India Reference Rate Is Not Provided

There are cases where the Reserve Bank of India reference rate is not given, then the value for that foreign currency conversion transaction will be:

1% of the amount (gross) which is supplied or received by the transacting person.

If we consider the above example, Mr X is the transacting person here. He is purchasing or selling 100 USD, wherein 1 USD ₹84. The gross amount is ₹8400.

The value of supply, which is 1% of 8400= ₹84

Therefore, tax on forex at the applicable rate= 84*18%= ₹15.12

Case 2: When Both Currencies Being Exchanged are Foreign Currencies

When both currencies being exchanged are foreign currencies, the value of the supply of services is:

1% of the lesser amount (calculated after converting both currencies to INR)

Let us understand this better with an example:

Mr. X wishes to sell off 100 USD for the UK pound at the rate of 0.92 pounds per USD. The value, in this case, will be 92 pounds.

On converting both currencies into INR:

100 USD = ₹8,400 (at ₹84 per USD)

92 Pound = ₹10,120 (at ₹110 per Pound)

The taxable supply value is 1% of the lesser amount, 1% of 8,400= ₹84

Therefore, the Goods and Services Tax on currency exchange conversion is 84 * 18% = ₹15.12

Method 2: Slab Based Under Rule 32(2)(b) of CGST Rule, 2017

You can also calculate the value of supply based on some predefined rules. Take a look at the table below to understand this better:

| Sl.No | Gross Amount of Foreign Currency Exchanged | Value of Supply | ||

| (A) | (B) | Result | ||

| 1. | Amount till 1,00,000 | 1% of the gross amount of foreign currency exchanged | ₹250 | The higher one (A) or (B) |

| 2. | Amount more than ₹1,00,000 and till ₹10,00,000 | 0.50% of the (total currency amount exchanged minus 1,00,000) | ₹1,000 | A + B |

| 3. | Amount more than 10,00,000 | 0.10% of the (total currency amount exchanged minus 10,00,000) + ₹ 5,500 | ₹60,000 | The lower one (A) or (B) |

For instance, if it amounts to ₹4,000, then the value of supply will be considered higher at either 1% of 4,000 (i.e. ₹40) or ₹250. Therefore, it is ₹250.

Conclusion

Understanding GST on foreign exchange is essential for both individuals and businesses. While GST does not apply to all transactions, certain forex transactions are subject to specific exchange rates and rules. A clear understanding of the topic will help you manage your finances and comply with tax regulations.

💡If you want to streamline your payment and make GST payments, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

Is GST applicable on inward remittances to India?

No, GST is not applicable on inward remittances to India because export of goods and services is treated as a zero-rated supply under GST law. However, some online platforms might charge an 18% fee for processing international money transfers, but this is not a GST charge on the remittance itself. Always verify any fees to avoid confusion.

How is GST calculated on foreign currency conversion in India?

GST on foreign currency conversion is based on a slab system. For amounts up to ₹1 lakh, 1% of the gross value is charged, subject to a minimum of ₹250. For amounts between ₹1 lakh and ₹10 lakh, 0.5% is charged on the amount exceeding ₹1 lakh plus ₹1,000. For amounts above ₹10 lakh, 0.1% is charged on the amount exceeding ₹10 lakh plus ₹5,500, with a maximum limit of ₹60,000.

What is the difference between currency conversion with and without the RBI reference rate?

When the RBI reference rate is available, GST is calculated on the difference between the reference rate and the buying/selling rate. If the RBI reference rate is not provided, the taxable value of the service is 1% of the gross amount exchanged. In both cases, GST is charged at 18% on the taxable value of the service.

Are services related to FIRC and BRC subject to GST?

Yes, services related to Foreign Inward Remittance Certificate (FIRC) and Bank Realisation Certificate (BRC) are subject to GST. The reverse charge mechanism applies here, meaning foreign clients are responsible for paying the GST directly to the Indian government. Therefore, businesses do not need to charge GST on invoices for these services.

How is GST calculated when both currencies being exchanged are foreign currencies?

When both currencies in a foreign exchange transaction are foreign, the taxable value of the service is 1% of the lesser amount after converting both currencies to Indian Rupees. For example, if 100 USD is exchanged for UK pounds, and the INR value of 100 USD is ₹8,400 while 92 pounds is ₹10,120, GST is calculated on ₹8,400, the lower amount, at 18%.

Read More About GST

5")

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction