Form GST RFD 03: GST Refund Deficiency Memo

Bio

Sandipan Mitra is the CEO and co-founder of Pice. He boasts eight years of experience in the B2B and fintech sector. Sandipan's journey includes significant roles at multiple Indian Unicorns Including Product at PayU, and as founding member / VP, Product at Open Financial Technologies.

- 17 Sep 25

- 6 mins

Share

Form GST RFD 03: GST Refund Deficiency Memo

- 08 Mins

- 17-09-25

Table of Contents

- What Is Form GST RFD-03?

- Who Issues Form GST RFD-03?

- When Can I Expect to Receive Form GST RFD-03?

- What Kind of Information Is Provided in Form GST RFD-03?

- What Is the Main Implication of Receiving Form GST RFD-03 for a Refund Claim?

- What Are Some Common Reasons Why a Taxpayer Might Receive Form GST RFD-03?

- What Is the Required Action After Receiving Form GST RFD-03?

- Does Receiving Form GST RFD-03 Extend the Time Limit to File the Refund Claim?

- How to Avoid GST RFD-03?

- Conclusion

Share

Key Takeaways

- Form GST RFD-03 is issued by tax officers when discrepancies are found in a taxpayer’s refund application.

- Receiving GST RFD-03 notice means the original refund claim is invalid, and a fresh corrected application must be filed.

- Common reasons for RFD-03 issuance include missing documents, incorrect bank details, and mismatches in GST returns.

- The refund claim time limit of 2 years remains unchanged even after receiving RFD-03 from tax authorities.

- Taxpayers can avoid GST RFD-03 deficiency memos by ensuring accurate documents, proper details, and timely submissions.

Form GST RFD-03 is issued by the tax officer if there are discrepancies in refund claims by a taxpayer. If the tax officer issues this form, you need to raise a new refund claim with rectified errors. Learn in detail about this form to avoid errors and discrepancies in your refund claims.

What Is Form GST RFD-03?

Tax officers verify GST RFD-01 refund claims that taxpayers file. If any discrepancies are found, such as missing documents, incomplete details, incorrect bank or invoice information, they issue a GST RFD-03 notice within 15 days of filing.

In such an instance, taxpayers need to submit a new refund application with corrections. As a result, it results in delayed reimbursements for businesses, in the process.

Who Issues Form GST RFD-03?

Tax officers issue GST RFD-03 if they identify discrepancies in GST RFD-01, filed by taxpayers. If you are a taxpayer, following the issuance of GST RFD-03, you need to raise a fresh refund application.

Must reads

When Can I Expect to Receive Form GST RFD-03?

In case there are discrepancies in the GST RFD-01 refund application, the tax officer will issue GST RFD-03 within 15 days of filing the application. As a result, you can expect it within 15 days, solely if there are discrepancies.

What Kind of Information Is Provided in Form GST RFD-03?

Here is the information contained in Form GST RFD-03:

● It contains the unique reference number of the original refund application.

● This form entails the date when the refund application was submitted.

● It contains the GSTIN and name of the taxpayer.

● This form contains the tax period and the reason for the refund.

● It contains a list of errors or reasons stating why the application is considered incomplete/incorrect.

● This form entails the sections or rules under which the deficiency is raised.

What Is the Main Implication of Receiving Form GST RFD-03 for a Refund Claim?

Here are the implications of GST RFD-03:

● The original refund application initially filed by a taxpayer is not processed further.

● Taxpayers need to raise a fresh refund application with corrections, upon receiving GST RFD-03 from the tax authorities.

● The initial time limit of 2 years remains applicable wherein taxpayers have to file a fresh application.

● In the case of GST RFD-03 issuance by tax authorities, the amount debited from the taxpayer's Electronic Credit Ledger or Electronic Cash Ledger is re-credited automatically.

What Are Some Common Reasons Why a Taxpayer Might Receive Form GST RFD-03?

Here are the reasons for which GSTR RFD-03 is issued:

● If a taxpayer does not submit complete documents or statements.

● In case there is a discrepancy in data between GST returns like GSTR-1 and GSTR-3B with the refund application.

● If incorrect details are given in annexures or statements for specific refund types.

● In case bank account details are incorrect or not validated.

● If a taxpayer claims a refund under an incorrect category.

● The application has issues with time while it was accepted initially in the system.

● If the taxpayer fails to provide relevant declarations or certificates like Chartered Accountant or Cost Accountant certificates, if necessary.

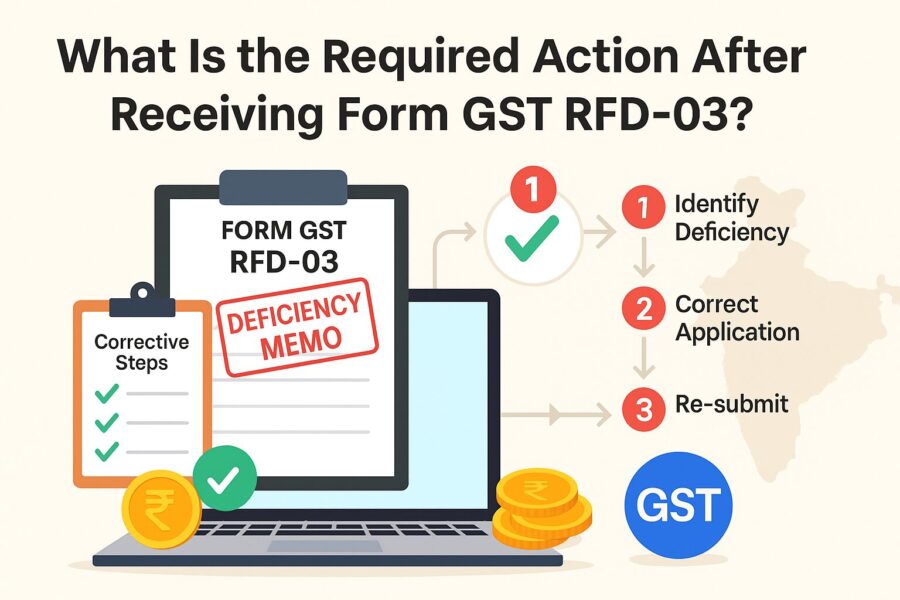

What Is the Required Action After Receiving Form GST RFD-03?

As a taxpayer, if you receive GST RFD-03 from the tax authorities, you need to review the discrepancies and errors. Further, you need to amend the errors in a fresh refund application and submit them to the tax authorities. You cannot amend the errors in the previous refund application.

Does Receiving Form GST RFD-03 Extend the Time Limit to File the Refund Claim?

Receiving GST RFD-03 does not extend the time limit of the refund claim. The refund time limit remains 2 years wherein taxpayers need to file the refund claims.

Must reads

How to Avoid GST RFD-03?

You can avoid GST RFD-03 by following the ways mentioned below:

● Read through Rule 89(2) before you submit the documents. In addition, provide accurate details in the form to avoid discrepancies.

● Ensure you track the refund status through frequent monitoring.

● Communicate with the GST officer to know about the refund claims.

● If needed, seek professional assistance to avoid deficiency memos.

Conclusion

Form GST RFD-03 does not provide any extension to the refund claim timeline. Therefore, it is important to follow the deadlines to receive your refund within the prescribed time. Timely tax refunds can enhance your business's cash flow and support seamless operations.

To prevent the issuance of GST RFD-03, make sure that all the details and documents submitted are accurate and complete. Double-check everything before submission to ensure nothing is missed.

💡If you want to streamline your payment and make GST payments via credit, debit card or UPI, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

What is Form GST RFD-03?

Form GST RFD-03 is a deficiency memo issued by the GST officer when errors, missing documents, or discrepancies are found in a refund application (RFD-01). It notifies the taxpayer about the issues that must be corrected. Once issued, the original refund application is considered invalid, and the taxpayer must file a fresh claim with corrections.

When is GST RFD-03 issued?

RFD-03 is issued within 15 days of filing a refund application (RFD-01) if the officer detects mismatches or deficiencies. These may include incorrect invoices, incomplete statements, bank detail errors, or data mismatches between GSTR-1 and GSTR-3B. Its purpose is to ensure refund applications are accurate before being processed further.

What should a taxpayer do after receiving RFD-03?

After receiving RFD-03, the taxpayer must review the reasons for rejection, correct the errors, and then file a new refund application. The earlier application cannot be modified. Importantly, the statutory 2-year time limit for filing refund claims remains applicable, so corrections should be made promptly to avoid losing eligibility.

Does receiving RFD-03 affect the refund claim timeline?

No, receiving GST RFD-03 does not extend the refund claim timeline. The refund must still be filed within 2 years from the relevant date as prescribed under GST law. This makes it critical for taxpayers to quickly identify and resolve discrepancies so that the fresh application is filed within the valid time frame.

How can businesses avoid getting GST RFD-03?

Businesses can avoid RFD-03 by ensuring complete and accurate documentation before filing refund claims. This includes validating bank details, reconciling GSTR-1 and GSTR-3B data, attaching required certificates (CA/Cost Accountant, if applicable), and verifying refund categories. Regular tracking of refund status and seeking professional GST assistance can also minimize errors and deficiency memos.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction