Form GST RFD 04: Provisional Order for Refund

Bio

Ankit Rahangdale is a seasoned finance professional with a distinguished background as a Chartered Accountant. Currently, he leads the Finance Department at Pice. With over five years of invaluable experience in the banking and finance sector, honing his expertise through esteemed institutions such as ICICI Bank and Standard Chartered Bank.

- 17 Sep 25

- 6 mins

Share

Form GST RFD 04: Provisional Order for Refund

- 08 Mins

- 17-09-25

Key Takeaways

- Form GST RFD-04 enables taxpayers to claim a provisional refund of up to 90% before final verification.

- Provisional refund under GST RFD-04 ensures liquidity for exporters and SEZ suppliers with zero-rated supplies.

- Businesses can apply for GST provisional refund through Form RFD-01, followed by RFD-04 sanction.

- The eligibility for RFD-04 depends on a clean compliance record without major tax evasion cases.

- Filing Form RFD-04 in GST helps maintain working capital while awaiting final refund approval.

Form GST RFD-04 plays a crucial role in India’s Goods and Services Tax (GST) refund mechanism by enabling provisional refunds to taxpayers. Form GST RFD-04 is the provisional refund application form in GST. When a business files a refund claim, this form allows them to receive up to 90% of the eligible amount even before the final verification is complete.

This provisional refund process, as outlined in Section 54(6) of the CGST Act, 2017, is particularly beneficial for exporters and suppliers to SEZs, helping them maintain liquidity and operational efficiency. The issuance of RFD-04 ensures timely disbursement of funds, aiding businesses in preserving working capital during the ongoing refund assessment.

So, learn about the applicability and process of using this form for a refund in GST on a provisional basis.

What Is a Provisional Refund Order?

Even if the GST review process is pending, you can use the Provisional Refund Order to accelerate refund in GST payments. Until complete claim verification is complete, businesses can use this method to receive a partial refund. As a result, this process improves the cash flow for businesses.

Section 54(6) of the CGST Act, 2017 (Central Goods and Services Act), states that businesses can acquire up to 90% of their refund as initial reimbursement. The remaining portion is released on completion of successful verification.

A business can qualify for an advance refund if they submit Form GST RFD-04 with their refund application. The concerned GST officers reserve the right to assign up to 90% refund in advance. This helps businesses preserve their working capital during the concerned assessment period.

The ultimate refund is processed on GST RFD-06 or rejected in GST RFD-08. In case there is a discrepancy in provisional and final refund, it needs to be followed by adjustments. Further, if there is a rejection, businesses need to restore the previously granted refund.

Usually, the tax authorities provide provisional refunds if businesses are involved in exports of goods and services or supplies to SEZ (Special Economic Zone) units and developers, which are zero-rated supplies.

Moreover, a proper officer provides a refund claim in GST without input tax credit adjustments. It takes 7 days or less to transfer funds to the taxpayer's account with Form RFD-05 payment advice in accordance with Form RFD-02. Notably, if a taxpayer has faced tax evasion charges of more than ₹2.5 Crore over the last 5 years, he/she will not be able to avail provisional refund.

Eligibility Criteria for Provisional Refunds

Here is the eligibility criteria for provisional refund in GST:

- If a taxpayer does not have a tax evasion history exceeding ₹2.5 Crore over the previous 5 years.

- In case the internal auditors rate the performance of a business at 5 or higher on the given scale.

- If the business does not have any pending legal case about a refund petition.

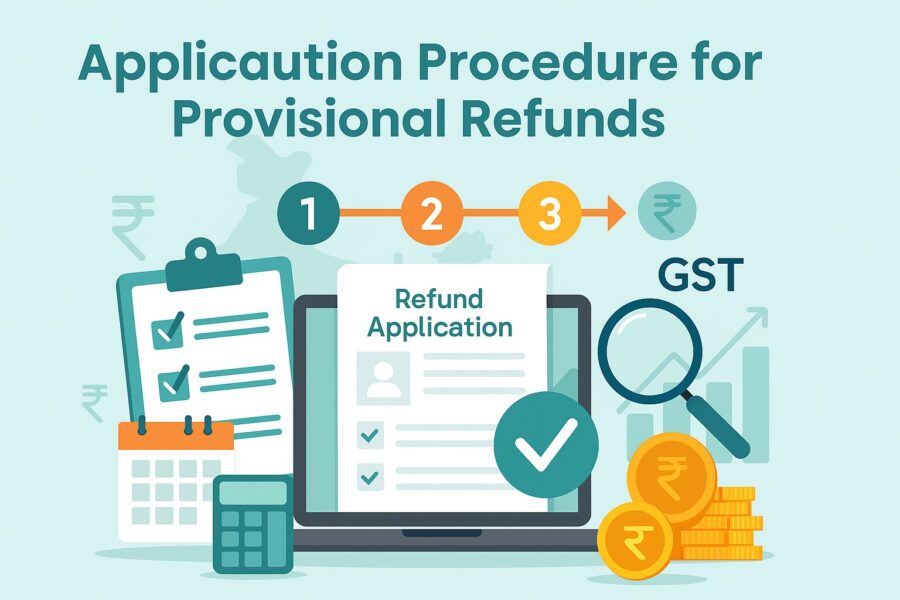

Application Procedure for Provisional Refunds

Here is the application process for provisional refunds:

1. Filling in the Refund Application: You need to provide all necessary information and documents in Form GST RFD-01 to claim refunds online on the GST portal.

2. Acknowledgment of Your Application: You will receive an acknowledgement number within 15 days from the date of application. Ensure you track the application using the number.

3. Review of Your Application: The GST officer will review your application and issue GST RFD-03 within 15 days if details are missing, incorrect or inappropriate.

4. Provisional Refund Approval: If all the information and documents are correct, the tax officer will issue a 90% provisional refund which will reach the taxpayer’s account within 7 days.

5. Final Refund Decision: Within the next 60 days, the GST officer will accept or reject your refund request based on evaluation and assessment. If accepted, you will receive the remaining amount in your bank account. In case the request is rejected, it will reflect on your credit ledger or offset your tax liabilities.

Form RFD-04 Issuance Cases

Here are the instances when RFD-04 is issued:

- Export of service with tax payment.

- Refund of ITC on export of goods or services under LUT/Bond without integrated tax payment.

- Supplies to SEZ units or developers with or without tax payment.

Details of Form RFD-04

Here are the details of the form:

● Sanction order number

● ARN (Application Reference Number) with date

● Acknowledgement number followed by the date

● A table containing the sanctioned amount and bank account details.

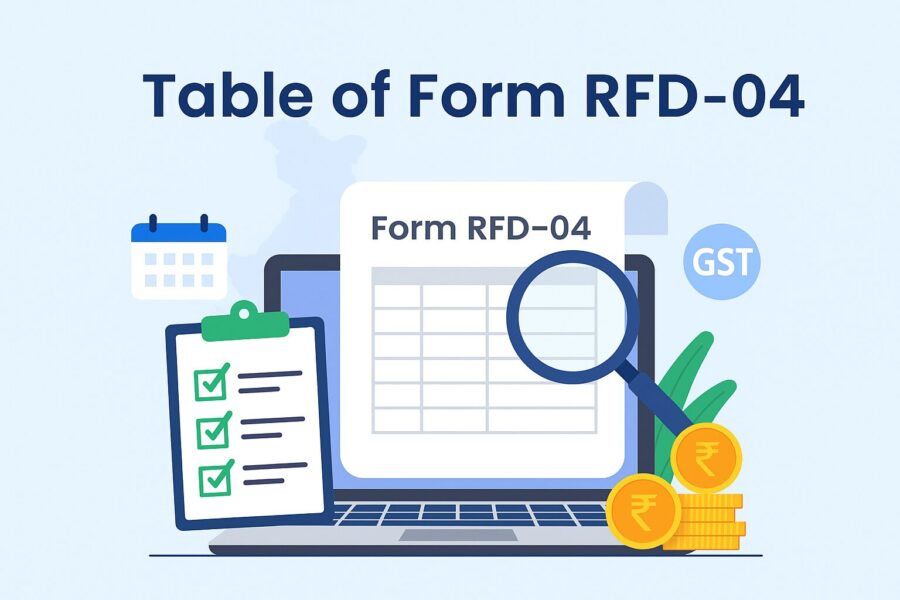

Table of Form RFD-04

Here are the details of the table of Form RFD-04:

● The refund amount claimed

● 10% of the refund amount which is sanctioned upon verification

● The balance amount, or 90% of the refund amount

● Amount of refund that has been sanctioned

● The bank account provided in the application

● Bank name

● Bank address

● IFSC code of the bank branch

● MICR of the branch

Conclusion

Form GST RFD-04 allows taxpayers to ensure smooth cash flow while a GST refund is in process. This helps them preserve their working capital while final refunds are sanctioned.

However, if there is a discrepancy in provisional and final refund, you need to adjust the same as a taxpayer to comply with Indian GST laws. Ensure you submit Form RFD-04 if you wish to claim a provisional refund.

💡If you want to streamline your payment and make GST payments via credit, debit card or UPI, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

What is Form GST RFD-04?

Form GST RFD-04 is the provisional refund order issued by GST authorities, allowing taxpayers to claim up to 90% of eligible refunds before final verification. It helps businesses, especially exporters and SEZ suppliers, maintain cash flow during refund processing.

Who can apply for a provisional refund using RFD-04?

Taxpayers engaged in exports of goods or services, or supplies to SEZs can apply for provisional refunds. However, they must not have a history of tax evasion exceeding ₹2.5 crore in the last 5 years, and no pending legal disputes related to refund claims.

How is the RFD-04 provisional refund process carried out?

The process starts with filing Form RFD-01 on the GST portal. Once verified, the GST officer issues RFD-04 within 7 days, granting 90% of the refund. The balance 10% is sanctioned later through RFD-06, after final assessment of the refund claim.

What happens if there is a mismatch between provisional and final refunds?

If discrepancies arise between RFD-04 (provisional) and RFD-06 (final) refunds, adjustments are made by the GST department. Any excess refund received must be paid back, while eligible balance amounts are credited to the taxpayer’s bank account.

How long does it take to get a provisional refund under RFD-04?

Once the refund application is submitted and verified, the GST officer issues RFD-04 within 7 days. The provisional refund is then credited to the taxpayer’s account through RFD-05 payment advice, ensuring quick liquidity during the verification stage.

Read More About GST

About the author

Key Takeaways Earn 3 reward points on every ₹100 spent....

0

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction