DRC 23 in GST: Release of Provisional Attachment of Property

Bio

An Alumnus of IIM and DU with almost a decade of experience in the banking and finance sectors. I had the opportunity to work with all types of institutions in BFSI ecosystem like Bank, NBFC, Fintech, Consulting and Auditor. I started my professional journey at KPMG and subsequently worked in leading names of the BFSI sector including Ujjivan Bank, Vistaar Finance. Currently building a fintech startup ( PICE) by handling alliances, compliance and creation of GTM strategy for payments and credit product.

- 17 Jul 25

- 6 mins

Share

DRC 23 in GST: Release of Provisional Attachment of Property

- 08 Mins

- 17-07-25

Key Takeaways

- Form GST DRC-23 is issued to revoke a provisional attachment order made under Section 83 of the CGST Act.

- It allows the release of attached property or bank accounts once the tax officer is satisfied that attachment is no longer necessary.

- The property is released upon payment of the lesser of its market value or the pending GST dues, with proof of payment.

- DRC-23 ensures fairness in recovery proceedings and protects taxpayers from arbitrary or unjustified attachments.

- Taxpayers can file objections within 7 days of attachment and seek release if the attachment lacks valid grounds.

The Central Board of Indirect Taxes and Customs (CBIC) has issued guidelines regarding the provisional attachment of property under Section 83 of the CGST Act, 2017. Such attachment may be carried out to secure or safeguard the recovery of tax dues under the GST law.

If the property is found to be, or is no longer, liable for attachment, the government may release it by issuing an order in Form GST DRC-23.

This blog focuses on what is a demand and recovery case, while highlighting all the associated details you need to know about DRC-23 in GST.

What Does Demand and Recovery Under GST Mean?

Under the GST regime, demand and recovery provisions come into effect when a taxpayer fails to pay the tax due. This could result from default, fraud or even a genuine mistake. Section 83 of the CGST Act empowers tax officers to provisionally attach a taxpayer's property, which includes the attachment of a bank account, to protect government revenue during such proceedings.

Taxpayers can use Form DRC-22 to execute the order, but if they successfully justify their case or if the officer finds no further need for the attachment, Form DRC-23 is issued to revoke the order.

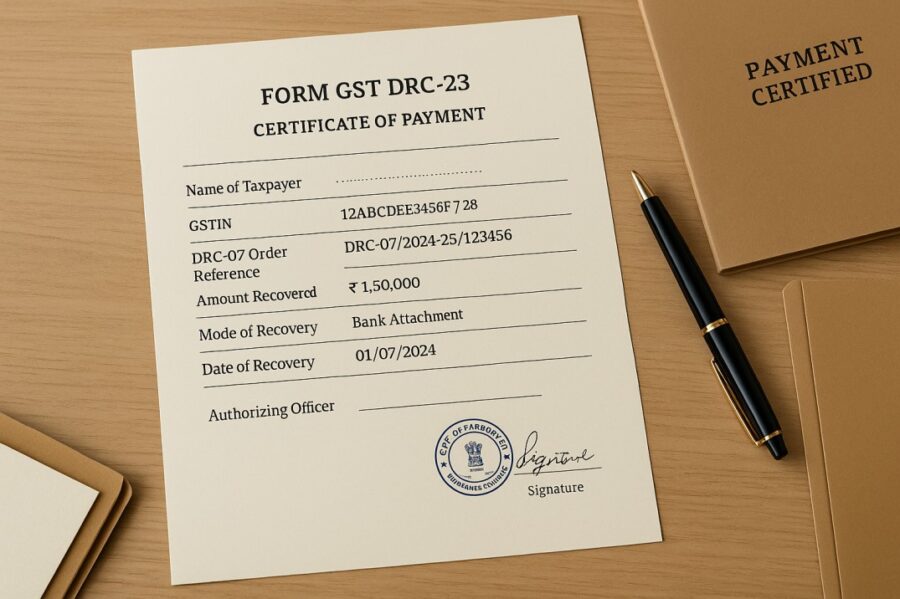

What is Form DRC 23 in GST?

While certain specified proceedings are ongoing, the Commissioner has the authority to issue an order for the attachment of a taxpayer's property to safeguard the interests of the revenue. The Commissioner can release such property by issuing an order via the DRC-23 form.

This release is subject to the condition that the taxable person pays an amount equal to the market value of the property or the amount payable (or likely to become payable) under the GST Act, whichever is lower. The taxable person must also submit proof of such payment before the property is released.

Must reads

Format of DRC 23 in GST

The DRC-23 form usually includes the following details:

- A reference to the earlier attachment order (DRC-22).

- The name and address of the bank or institution involved

- A confirmation that there is no longer any need for the attachment of bank accounts.

- The signature and designation of the Commissioner or authorised officer.

This form serves as an official instruction, which allows the smooth release of the bank account or any other attached property and restores normal business operations.

Is There Any Protection Against Arbitrary Attachments?

One growing concern among businesses is the trend of arbitrary bank attachments, even when no major default exists. While the law allows for attachment, it also requires that there be a valid reason and a fair approach.

Taxpayers can challenge any misuse of this power. Voluntary taxpayers should be aware that taking such actions is not to be done lightly.

DRC 23 in GST acts as a safeguard in the system, ensuring that unjustified attachments can be undone once the facts are clear.

Conclusion

Upon receipt of DRC-22, the voluntary or compulsory taxpayer may file an objection within 7 days of property attachment, stating that it was not liable for attachment. The Commissioner must provide a hearing, and if satisfied with the response, can release the property by issuing an order in Form DRC-23 in GST.

💡If you want to streamline your invoices and make payments via credit or debit card or UPI, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

What is Form GST DRC-23 and when is it issued?

Form GST DRC-23 is an official order for revoking the provisional attachment of a taxpayer’s property or bank account. It is issued by the Commissioner or an authorised officer when it is determined that the property is no longer required to be attached under Section 83 of the CGST Act. This usually happens after a taxpayer files an objection or clears the dues as per the law.

What are the conditions for releasing property through Form DRC-23?

To obtain a release through Form DRC-23, the taxpayer must submit proof of payment of either the market value of the attached property or the outstanding tax amount, whichever is lower. Once this is verified and the officer is satisfied that attachment is no longer necessary, the release order is issued. This helps resume normal banking or business operations for the taxpayer.

How does DRC-23 relate to the earlier issued DRC-22?

Form DRC-22 is issued to provisionally attach a taxpayer’s property during recovery proceedings. If the taxpayer successfully disputes the attachment or clears the outstanding dues, the same officer may issue Form DRC-23 to revoke the attachment. DRC-23 thus acts as a corrective step to restore access to the property or account once the revenue risk is mitigated.

Can a taxpayer object to a provisional attachment under GST?

Yes, the taxpayer has the right to file an objection within 7 days of receiving a DRC-22 notice. They can contest the attachment by presenting valid reasons and supporting evidence. If the Commissioner is convinced during the hearing that the attachment was unnecessary, they may issue a Form DRC-23 to revoke it. This ensures procedural fairness in the recovery process.

Does Form DRC-23 provide protection against arbitrary bank attachments?

Yes, DRC-23 serves as a safeguard against unwarranted or arbitrary attachments under GST. While the government has the power to attach assets provisionally, this must be backed by valid reasons. If found unjustified, DRC-23 allows for prompt revocation, ensuring that business operations are not unfairly disrupted. It strengthens the balance between enforcement and taxpayer rights.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction