Know about the GSTR 4 Return Format?

Bio

An Alumnus of IIM and DU with almost a decade of experience in the banking and finance sectors. I had the opportunity to work with all types of institutions in BFSI ecosystem like Bank, NBFC, Fintech, Consulting and Auditor. I started my professional journey at KPMG and subsequently worked in leading names of the BFSI sector including Ujjivan Bank, Vistaar Finance. Currently building a fintech startup ( PICE) by handling alliances, compliance and creation of GTM strategy for payments and credit product.

- 18 Mar 25

- 6 mins

Share

Know about the GSTR 4 Return Format?

- 08 Mins

- 18-03-25

Share

Key Takeaways

- Annual return for composition dealers under the GST scheme.

- Simplifies tax filing with auto-filled data from CMP-08.

- Captures inward & outward supplies, tax liabilities, and payments.

- Due by April 30th to avoid penalties.

- Refund option available for excess tax paid.

The GSTR-4 return format is designed for taxpayers registered under the GST composition scheme. It is an annual return that helps composition dealers simplify their tax filing process. The third amendment of the GST Act, 2017 enabled this return to capture essential information about inward and outward supplies, tax liability and payments of the financial year.

Businesses under the composition scheme need to learn the GSTR-4 structure so they can comply with GST regulations while enjoying a lowered tax charge.

What Is GSTR-4?

Form GSTR-4 was introduced through the third amendment of the GST Act, 2017. It is an annual return that must be filed by taxpayers registered under the GST composition scheme. This scheme is designed specifically for small and medium businesses, helping them lower costs by allowing GST payments at a fixed, reduced rate.

It includes details of their business transactions, covering supply details, sales and the total composition tax paid during the current tax period.

Who Should File GSTR-4?

Taxpayers who have opted for the composition scheme must file GSTR-4 by the 30th of April following the current financial year. Earlier, the due date was the 18th of the month following the end of a relevant quarter. This also includes service providers covered under the special composition scheme introduced through CGST (Rate) notification number 2/2019, dated March 7, 2020, applicable from the financial year 2019-20.

Must reads

What Is the GSTR 4 Return Format?

The GSTR-4 return format includes various details related to composition dealers. This updated annual Form GSTR-4 consists of 9 sections, capturing key details of composition taxpayers. Here is a detailed breakdown of the tables in form:

?feature=shared

?feature=shared

Tables 1-3: Basic Information

GSTIN: The GSTIN of a taxpayer is automatically filled in when filing returns after GST registration.

Name of the Taxpayer: The legal and trade names are pre-filled during the return filing process.

Aggregate Turnover Details: Your business’s aggregate turnover from the previous financial year is automatically captured. Additionally, the ARN and its date are updated after filing.

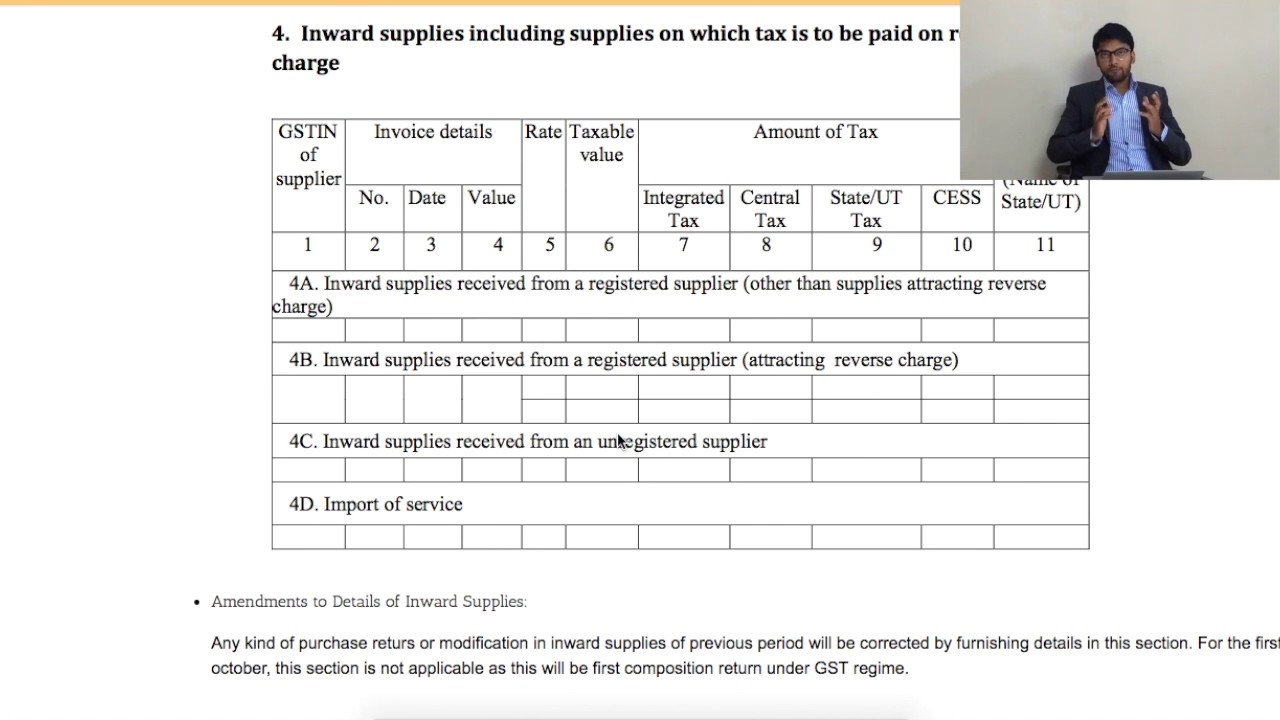

Table 4: Inward Supplies

Amendments to details on inward supplies reported in earlier tax period returns are mentioned in Table 4.

4A: Supplies from a Registered Supplier (Excluding Reverse Charge)

Taxpayers must report all purchases from registered suppliers, covering both interstate and intrastate transactions, where the reverse charge mechanism does not apply.

4B: Supplies from a Registered Supplier (Subject to Reverse Charge)

Taxpayers must disclose all purchases from registered suppliers, including both interstate and intrastate transactions, where the reverse charge mechanism applies.

4C: Unregistered Supplier

Taxpayers must report all purchases from unregistered suppliers, covering both interstate supplies and intrastate supplies.

4D: Import of Services

Taxpayers must provide details of imported services where tax liability arises due to the reverse charge mechanism.

Table 5: Summary of Self-Assessed Tax Liability as per Form GST CMP-08

The information in this table is automatically fetched from Form CMP-08 which is a quarterly return form, used for tax payments. Form CMP-08 quarterly statements consolidate details of payments made from all CMP-08 filings throughout the year, including payments for outward supplies, inward supplies subject to reverse charge, tax paid and any interest paid on late payments of tax.

Table 6: Outward Supplies

Composition taxpayers must report all outward supplies and inward supplies subject to reverse charge, categorised by tax rate, along with the total taxable value. The IGST, SGST, CGST, and cess amounts will be automatically populated.

Table 7: TDS/TCS Credit Received

Any TDS/TCS credit received from a supplier or e-commerce operator will be automatically filled in the table below. The taxpayer must provide the GSTIN of the deductor, the gross invoice value and the TDS amount deducted while filing this GST return form.

Table 8: Tax, Interest, Late Fee Paid And Payable

| Item | Details |

| Tax amount payable | This amount is automatically filled from Table 6 mentioned above. |

| Tax amount already paid | This is auto-filled based on the details in Form GST CMP-08. |

| Balance tax payable | It reflects the difference between the amounts in points 1 and 2 above. |

| Interest payable and paid | Any interest due for late annual return form filing and the amount actually paid are to be specified here. |

| Late fee payable and paid | This section captures the late fee due for delayed GST payment and the amount actually paid. |

| Amounts paid under various tax heads | Payments should be mentioned separately for IGST, SGST, CGST and cess. |

Table 9: Refund Claimed From Electronic Cash Ledger

If excess taxes have been paid, a refund can be requested using this table. The refund amount must be categorised into tax, interest, penalty, fee and other components. The taxpayer must verify and confirm that the information provided in the tables of the GSTR-4 form and check whether the declaration of truth is accurate by signing the form.

Conclusion

The GSTR-4 return format provides a structured approach for composition taxpayers to report their annual transactions. The 9-section format of this GST form simplifies GST related processes for small to medium enterprises through its functionality to record inward and outward supplies details together with self-assessed taxes and refund features.

Accurate filing of Form GSTR-4 allows composition dealers to uphold their tax duties in an efficient manner and receive discounted tax rates under the scheme.

💡If you want to streamline your payment and make GST payments via credit or debit card, UPI consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

Who needs to file GSTR-4?

GSTR-4 must be filed by taxpayers registered under the GST Composition Scheme, including small businesses and service providers under the special composition scheme. It is an annual return due by April 30th of the following financial year.

What details are required in GSTR-4?

GSTR-4 includes basic taxpayer details, inward and outward supplies, tax liability, tax paid, TDS/TCS credits, and refunds. Many fields are auto-filled based on previous CMP-08 filings.

What happens if GSTR-4 is not filed on time?

A late fee of ₹50 per day (₹25 each for CGST & SGST) applies, capped at ₹500 per return. If there is a tax liability, the penalty is ₹200 per day (₹100 each for CGST & SGST), with no upper limit.

Can excess tax be refunded in GSTR-4?

Yes, if excess tax has been paid, a refund can be claimed through the electronic cash ledger in Table 9 of the form. The amount will be categorized under tax, interest, penalty, and other charges.

How is tax liability calculated in GSTR-4?

Tax liability is auto-calculated based on outward supplies and inward supplies liable for reverse charge. It is pre-filled from Form CMP-08, which is filed quarterly for tax payments.

Read More About GST

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction