GST on Maintenance Charges by RWA

Bio

Sandipan Mitra is the CEO and co-founder of Pice. He boasts eight years of experience in the B2B and fintech sector. Sandipan's journey includes significant roles at multiple Indian Unicorns Including Product at PayU, and as founding member / VP, Product at Open Financial Technologies.

- 18 Feb 25

- 11 mins

Share

GST on Maintenance Charges by RWA

- 08 Mins

- 18-02-25

Table of Contents

- What Are Resident Welfare Associations?

- What Is GST?

- How GST on Maintenance Charges by RWA Works?

- How GST Is Applied to Resident Welfare Associations?

- Differentiating GST Applicability for Various Types of RWAs

- GST Registration for RWAs

- Input Tax Credit (ITC) for RWAs

- How RWAs Can Do Tax Calculations?

- Which GST Returns Are Applicable to RWAs?

- How GST Has Impacted RWA’s Financing and Budgeting?

- Conclusion

Share

Key Takeaways

- GST Applicability: RWAs pay 18% GST if maintenance per member exceeds ₹7,500 and turnover is over ₹20 lakh.

- Exemptions: RWAs below ₹20 lakh turnover or charging ₹7,500 or less are GST-exempt.

- ITC Benefits: RWAs can claim Input Tax Credit (ITC) on eligible expenses like security and housekeeping.

- GST Compliance: Timely filing of GSTR-1, GSTR-3B, and GSTR-9 avoids penalties.

- Financial Impact: GST increases costs, requiring better budgeting and record-keeping.

Resident Welfare Associations are a common sight across major cities in India. They are responsible for looking after the needs of the residents and flat owners who live in a particular society.

RWAs work as non-government organisations and ensure delivery of important services such as garbage collection, water supply and organising events at a residential complex. In case of any problems, they are responsible for resolving them.

In return for their services, they claim maintenance charges from the residents. But do you know that the government imposes GST on maintenance charges by RWA? In this blog, we will discuss which RWAs are subject to GST, how RWAs can calculate their GST returns and the due date for filing different GST returns.

What Are Resident Welfare Associations?

An RWA is a body which voices the concerns of the residents of a housing society, apartment complex, residential complex, etc. The Societies Registration Act of 1860 governs their work. An RWA must have at least 7 members and the age of each member must be above 18.

One of the most common and important functions of an RWA is to ensure the cleanliness and maintenance of amenities of the housing area. For this, they collect maintenance charges for residents. In the rest of the blog, we will cover the GST on maintenance charges by RWA.

What Is GST?

Goods and Services Tax (GST) is a major effort to unify the indirect taxes in India. It represents the agenda of “One Nation, One Tax”. The Union Government introduced the GST to simplify the taxation of goods and services across India.

Must reads

How GST on Maintenance Charges by RWA Works?

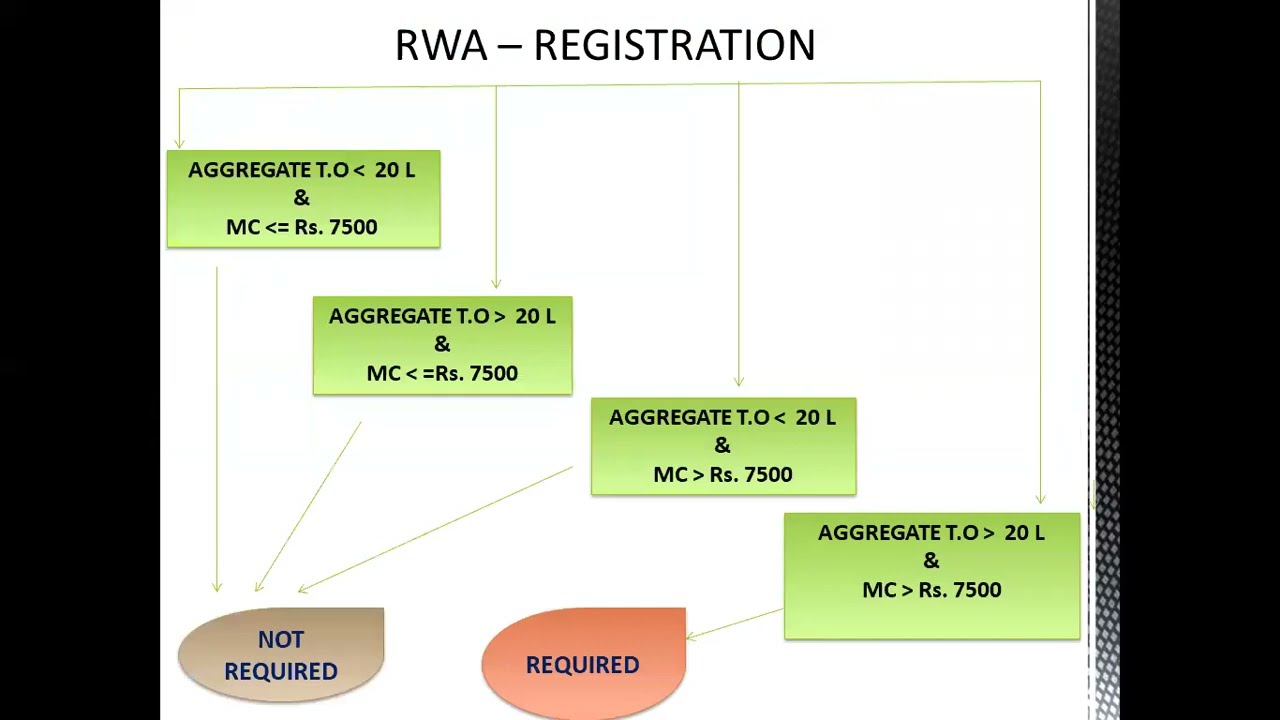

The Finance Ministry released circular 109/28/2019- GST to clarify the rules regarding the application of GST on maintenance charges imposed by Resident Welfare Associations.

As per the circular, residents paying up to ₹7,500 monthly as monthly maintenance charges will not face GST. Earlier, the limit was set at ₹5,000. It was increased to ₹7,500 on 25 January 2018.

Moreover, if the aggregate turnover of the RWA is up to ₹20 lakh, then the maintenance changes paid by the residents will be exempt from GST. The exemption will be valid even if the residents pay more than ₹7,500 monthly as maintenance charges.

GST is applied to maintenance charges when the charge per member exceeds ₹7,500 and the Resident Welfare Association’s turnover exceeds ₹20 lakh. The GST rate for the maintenance charges is 18%.

Here’s a simplified breakdown of the cases in which the GST on maintenance charges is applicable:

| Annual Turnover of RWA | Monthly Maintenance Charges | Applicability of GST on Maintenance Charges |

| Over of ₹20 lakh | Over ₹7,500 | Yes |

| ₹7,500 or less | No | |

| ₹20 lakh or less | Over ₹7,500 | No |

| ₹7,500 or less | No |

?feature=shared

?feature=shared

How GST Is Applied to Resident Welfare Associations?

As per the GST rules, any supply of goods and services from one person to another is subject to GST.

RWAs are responsible for providing various services to the housing area they represent. Since RWAs provide services in return for maintenance charges paid by the residents, their services are subject to GST. Some of the services offered by RWAs which are subject to GST include:

- Housekeeping, maintenance and providing amenities

- Security

- Payment of utility bills if it is paid out of a maintenance fund

- Water supply charges

- Booking hall for public gatherings

Differentiating GST Applicability for Various Types of RWAs

The application of GST varies according to the type and size of the RWA. Here’s a look at the different types of RWAs for applying GST:

- Self-Managed Small RWAs

A small RWA is considered to be self-managed if it is managed directly by the members without hiring any staff or outsourcing any of the work. They usually have less than 25 to 30 members. These RWAs are usually found in cooperative housing societies and small apartments.

They usually have minimal amenities and collect a small amount as maintenance charge. Since no services are provided formally, these RWAs are exempt from GST requirements. Thus, they are not burdened with filing returns and providing tax invoices.

- Large RWAs Whose Turnover Exceeds the GST Threshold

RWAs of large housing societies have high expenses. They have to pay their staff, take care of administrative and maintenance costs, and contract security services. If the annual turnover of such a large RWA exceeds the annual turnover limit of ₹20 lakh, then it will have to fulfil all GST requirements such as filing returns on time.

Such an RWA must register for GST and pay GST for all the services rendered by it. The maintenance charges collected by the RWA will be used for paying the GST.

- RWAs Whose Services Extend Beyond the Housing Society

While RWAs are primarily connected with serving the members of the housing society which they represent, they may also provide services to outsiders. For example, they may rent out a garden or community hall. They may also sell products to outsiders. The applicable GST rate will vary according to the service.

The income generated from selling such goods and services is subject to GST. Threshold exemption rules don’t apply in this case.

- Commercial Outlets on RWA Premises

Often shops, restaurants, medicine shops and convenience stores are set up within a housing society. These entities must be GST-compliant. The RWA must ensure that such commercial outlets are registered for GST collection and file their returns.

Must reads

GST Registration for RWAs

An RWA has to register for GST if its aggregate turnover exceeds ₹20 lakh. For special category states, the threshold limit is ₹10 lakh. For applying GST on RWAs, the aggregate turnover covers:

- The tax applies to all goods and services sold

- GST-exempted goods and services

- Goods and services which have been exported

- Inter-state supply of goods and services

Here are some of the important points to remember regarding GST for RWAs:

- GST registration is mandatory for all RWA whose turnover crosses the ₹20 lakh threshold

- An RWA can register voluntarily even if it is below the threshold

- Registered RWAs can claim input tax credit (ITC) for providing taxable goods and services

- The GST registration can be done on the GST portal. For the registration, the RWA must submit the required documents and information.

Input Tax Credit (ITC) for RWAs

While paying GST, a business could end up paying GST both on its input services and the output it sells by using this input. This leads to a cascading of taxes. To avoid the losses due to paying multiple taxes for the same thing, input tax credit (ITC) is used. It helps in reducing the tax burden.

ITC allows a business to get back the GST paid on an input if GST has already been paid on the output produced with this input. The same can be claimed by RWAs as well.

The following are some of the things RWAs can claim ITC on:

- Inward Supplies: It covers the GST RWAs pay on supplies they receive from outside.

- Capital Goods: GST paid on buying equipment, furniture, tools, etc.

- Input Services: Under this, GST which RWAs pay for services such as housekeeping and security are covered.

Here are some of the things RWAs must ensure to successfully claim ITC:

- They must keep the tax invoices for the goods they purchase from vendors.

- GST must be paid separately.

- ITC must be claimed on monthly GST returns.

Below you can find a list of common goods and services paid for by RWAs and whether they are covered by ITC:

| Good or Service | ITC Eligibility |

| Security | Eligible |

| Housekeeping | Eligible |

| Buying Generator | Eligible |

| Audit fees | Eligible |

| Property/water tax | Ineligible |

| Brokerage for buying flat | Ineligible |

How RWAs Can Do Tax Calculations?

In this section, we will look at how RWAs can perform tax calculations. The calculations are not necessary for exempted RWAs.

Here are the basic steps for calculating GST for registered RWAs:

- As per GST rate slabs, find out the taxable goods and services provided by the RWA.

- Add the CGST and SGST to the taxable amount.

- Subtract the applicable ITC from the CGST and SGST.

These steps will reveal the GST amount which the RWA must pay.

Must reads

Which GST Returns Are Applicable to RWAs?

The following GST returns are applicable to RWAs:

GSTR-1: It contains information about outward supplies and taxes.

GSTR-3B: It has information on monthly tax returns.

GSTR-9 : It comprises annual GST returns and contains records of ITC claims, refunds etc.

Late payments can lead to big penalties. Therefore, RWAs must file GST returns on time. The following table shows the due dates for payment of GST returns for different types:

| GST Return | Period | Due Date |

| GSTR-1 | Monthly | 11th of next month |

| GSTR-3B | Monthly | 20th of next month |

| GSTR-9 | Annually | 31st December |

How GST Has Impacted RWA’s Financing and Budgeting?

In this section, we will look at how GST has influenced the financing of RWAs. We also look at the challenges for RWAs.

- Increased Tax Liabilities

With the introduction of GST payments, RWAs now have to pay GST on the maintenance charges they collect from the residents. It increases their tax burden. If the residents do not pay greater amounts as maintenance charges, the RWAs will have to compensate for the increased taxation by controlling the goods, services and maintenance activities they offer. It leads to a reduction in the funds available for providing useful services.

- Strains Working Capital

Even though ITC solves the problem of GST liability cascading, it is available with a time lag. During the time duration between the payment of tax on input and finally getting the ITC, an RWA suffers from a shortage of money.

If the RWA has a tight budget, it may not be able to provide necessary goods and services to its residents. This problem would be solved only when it successfully claims the ITC.

- Cost of Compliance

RWAs have to bear the expenses for complying with GST implications. Typical expenses include buying accounting software, invoice generation, keeping records, consulting for tax-related issues etc.

An RWA may need to hire accounting staff to look after the calculation of GST, documentation, and filing of returns. Thus, the cost of compliance can reduce the funds at the RWA’s disposal.

- Budgeting

It is important for RWAs to prepare their budget with a higher tax burden in mind. They also have to account for inflation, greater compliance costs and improving services for flat owners.

They also need to think about the fees for tax consultation, registration, compliance etc. All this points to a need for more planning in budgeting. Therefore, budgeting plays a crucial role for RWAs.

- Greater Financial Responsibilities

GST has led to greater taxation, accounting, and compliance responsibilities for RWAs. Thus, it is important for them to be much more diligent in financial matters. RWAs must have higher standards for maintaining records and planning expenditures. Following the correct methods is important for claiming ITC benefits and avoiding any penalties.

Conclusion

GST represents a revolution in India’s taxation system. It sought to simplify the myriad indirect taxes in the country and make life easy for all Indians.

After reading this blog, you know about the GST on maintenance charges by RWA. While smaller, self-managed RWAs need not register for GST, the larger RWAs with turnover of more than ₹20 lakh must pay GST on their taxable services. GST is also applicable if the RWA provides services such as renting a community hall to third-parties.

RWAs need to show greater attentiveness when it comes to maintaining their financial records, collecting monthly maintenance fees and filing their GST returns on time. Late payments must be avoided. It will help them stay GST-compliant and avoid any penalties. If possible, RWAs can use abatement provisions to reduce their tax burden.

💡If you want to streamline your payment and make GST payments via credit card, consider using the PICE App. Explore the PICE App today and take your business to new heights.

FAQs

When does an RWA need to pay GST on maintenance charges?

An RWA must pay 18% GST if the maintenance charge per member exceeds ₹7,500 and its annual turnover is over ₹20 lakh. If either condition is not met, GST is not applicable.

Can an RWA claim Input Tax Credit (ITC)?

Yes, RWAs can claim ITC on eligible expenses like security, housekeeping, and capital goods. However, ITC is not available on property tax, water tax, or brokerage fees.

What are the key GST returns RWAs must file?

RWAs must file GSTR-1 (monthly sales details by the 11th), GSTR-3B (monthly tax summary by the 20th), and GSTR-9 (annual return by December 31st).

Are small RWAs required to register for GST?

No, RWAs with annual turnover below ₹20 lakh (₹10 lakh for special category states) are exempt from GST registration and compliance requirements.

How does GST impact an RWA’s finances?

GST increases tax liability, compliance costs, and working capital needs. RWAs must budget carefully, maintain records, and ensure timely GST payments to avoid penalties.

Read More About GST

: objectives of cst act 1956 2")

About the author

Key Takeaways Earn 1% cashback on all eligible transactions. The...

0

0

×

Want an answer to all your B2B Payment Problems?

Pay your Vendors and Collect from customers with ease using Pice's Payment Solutions. Get:

-

Instant Transfer

Instant Transfer

-

Lowest Rates

Lowest Rates

-

Credit on all transaction

Credit on all transaction